January 2018 isn’t just the deadline for PSD2’s adoption into national laws and regulation, it’s also the compliance deadline for the EU’s revamped ‘Markets in Financial Instruments Directive’ — otherwise known as MiFID II.

MiFID II is designed to make investment in a variety of asset classes safer and more transparent, including exchange traded funds, futures, foreign exchange and equities. The comprehensive regulatory update applies to everyone involved in the organised trading of these financial instruments in the EEA, from banks to exchanges, high-frequency traders, retail investors, fund managers and trading venues — as well as any non-European subsidiaries.

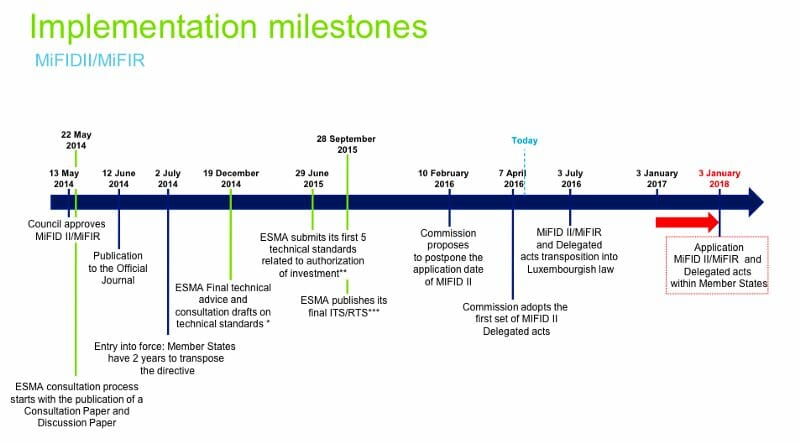

MiFID II Implementation Milestones — Deloitte

Improving on MiFID Legislation

The original MiFID legislation, rolled out in 2007, was a part of the EU’s broader mission of unifying the financial market so that it could more effectively rival that of the US. As well as improving the market’s resilience and transparency, it also aimed to drive down the cost of trading for investors, diminishing the dominance of stock exchanges and ultimately contributing to financial growth.

Critics of the 2007 legislation cited an exaggerated focus on equities and a lack of consideration for under-regulated aspects of the financial market — such as derivatives and bonds. The global financial crisis, with its over the counter (OTC) derivative exposure and trade scandals, made it clear that more strident legislation was in order.

Addressing these issues is one goal of MiFID II, as is adapting the regulation to address the great leaps in financial technology we’ve seen in the last decade.

“The strengths of FinTech startups include independence, MIFID II compliance from scratch, flexibility and ability to adapt to clients’ requests.” — Bertrand Mouchot-Chardin

MiFID II Key Areas of Change

In addition to increasing the scope of MiFID beyond equities, MiFID II incurs further requirements for compliance, including:

- Requirements for internal risk management and governance, including proof of qualification for senior management.

- Stricter controls on dark pool trading and algorithmic trading.

- Greater transparency in organised trading, including pre and post-trade requirements.

- Position limits for commodity derivatives.

- Investor protection, including the right for national supervisory bodies to put limits on the sale of certain financial instruments — or ban them entirely.

Bertrand Mouchot-Chardin, Director at Greenwich Dealing Luxembourg, believes these changes will force financial players to think outside the box and challenge them to adapt to a new landscape. “MIFID II has a direct impact on commercial models of traditional financial institutions,” Mouchot-Chardin says. “All investment firms and sell-side firms need to restructure and explore new models.”

MiFID II legislation is designed to push trades away from phones and into electronic venues for better surveillance. Institutions will be required to report trade data faster and more comprehensively.

But one of the most talked about changes is known as unbundling: Asset managers will no longer receive free research and analysis alongside their trading activity. This will require new ways of thinking on the part of institutions.

Thomas Beevers, StockViews

Thomas Beevers, Co-founder & CEO of StockViews Ltd, agrees. “We are seeing huge disruption in the market for institutional equity research, with many asset managers taking on costs of research for the first time. This is shifting the way research is valued and procured. Incumbent banks are still struggling to find the right pricing model, while a drive to quality means many providers of mediocre research will not find a market.”

MiFID II and Non-EU Markets

Although MiFID II is applicable only within the EEA, non-EU institutions will likely experience trickle-down effects of the legislation. Areas outside of the EU — most notably the US and Asia — must keep tabs on the legislation in order to comply and continue relationships on both the buy and sell-side.

Olivier Mathurin, AIM Software

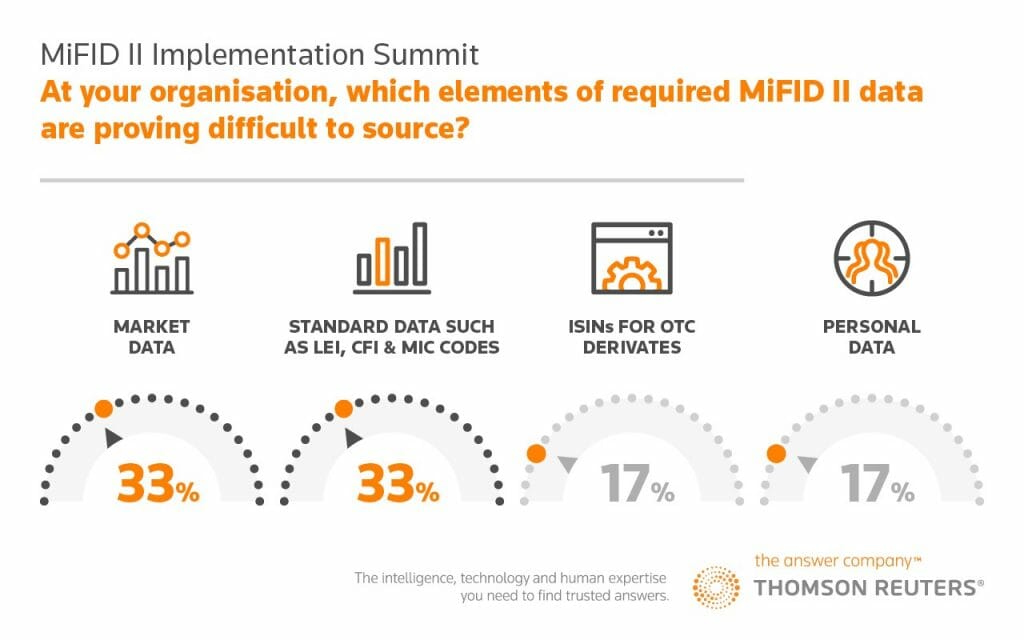

Many agree that data management and effective reporting are particular areas to note for non-EU financial institutions. Olivier Mathurin, Head of Strategic Research, AIM Software describes a potential competitive advantage for companies with strong presence outside the EU.

“MiFID II will be impacting not just European financial institutions, but also the non-European subsidiaries of these companies,” Mathurin says. “It will also be impacting different departments — trade, research, compliance. Different participants will be reporting at pre-trade, post-trade. Having consistent data will be a key advantage.”

More specifically, Mouchot-Chardin says that automated reporting technology will play a significant role.

“Firms need to develop a reporting service which automates the data gathering, analysis and reporting,” he says. “This obligation to report will also create opportunities for treatment of data passed through the trading life cycle in order to allow a better understanding of pricing and liquidity.”

Analyzing Opportunities in the Wake of MiFID II

While MiFID II comes with its own unique set of obstacles for banks and financial services, it also brings new opportunities. Much like how PSD2 has created pathways for startups and traditional institutions to gain competitive advantage with API-driven services, MiFID II also allows for this type of innovation — but it requires both progressive thinking and careful strategy.

John Liver, EY

“MiFID II is one of the key regulatory initiatives that will change market structure and business models,” says John Liver, Partner and Head of Global Regulatory Reform at EY. “Firms that manage the regulatory agenda as part of their strategic evolution and maintain flexibility will capture market opportunities in contrast to those that view implementation merely as a compliance task.”

Each type of financial institution will benefit from evaluating their existing infrastructure, as well as their unique strengths and weaknesses within the market. Legacy architecture can hold companies to ransom over their data, making compliance more painful and costly. It’s important that institutions take steps that go beyond compliance to elevate their competitive position.

“The lack of transparency of some traditional financial institutions may simply lead to the disappearance of long-established firms.” — Bertrand Mouchot-Chardin

“The strengths of FinTech startups include independence, MIFID II compliance from scratch, flexibility and ability to adapt to clients’ requests; but they also face costs related to regulation and technology and lack an established image,” says Mouchot-Chardin. “Traditional financial institutions, on the other hand, benefit from their position on the market but will not be able to provide tailor-made solutions at low prices. The lack of transparency of some traditional financial institutions may simply lead to the disappearance of long-established firms.”

Regtech startups can offer financial institutions valuable services that help them comply with new legislation, which is 1.4 million paragraphs and growing. Modern open architecture opens the door to a range of cutting edge Regtech solutions that can make compliance with existing regulation easier, as well as future-proof against regulatory change. Given the pace of change within the financial technology industry, it is likely that demands will continue to evolve, and smart Regtech solutions will evolve in line. A change in architecture may incur an unpleasant upfront cost, but it will likely save significant time and effort in the long term.

Having a straightforward route to compliance allows financial institutions to then focus on capturing the market in other ways. Trading venues, banks, and market infrastructure providers can work to develop scalable platforms that can handle smaller players, reduce the complexity involved and eliminate significant risks.

MiFID II: Moving Forward

As with most complex legislation, MiFID II does not offer clear-cut next steps or answers for financial institutions. However, now is the time for trading institutions, banks, investment funds and other firms to take a long and scrutinizing look at their infrastructure and operations. Only then will be able to make strides toward compliance, carve new niches in the market and move forward to potentially benefit from MiFID II in January.

For startups, the landscape is rich with opportunities. While the compliance side of MiFID II may be painful at the onset for those unprepared, we shouldn’t forget that these changes ultimately bring necessary innovation within the financial industry as a whole.

Will your MiFID II compliance be a seamless transition? — Thomson Reuters