At the LHoFT, we help founders with innovative ideas turn those ideas into startups with a transformative effect in the finance industry. We also help established startups expand into Europe and beyond, expanding their reach and market penetration.

In talking with founders who fall into the latter group, established and expanding, we have identified the three most significant concerns when attempting to scale after finding initial traction:

- Focus on the Numbers

- Strategic Agility

- Hire the Right People

To explain these issues, we consulted some local startup executives to share their insight and experience:

- Raoul Mulheims, Co-Founder & Chief Executive Officer of Finologee S.A

- Nicolas Buck, Chief Executive Officer of SEQVOIA

- Timothy Nuy, Executive Director and Dave Van Niekerk, Chief Executive Officer of MyBucks

1. Focus on the Numbers: KPIs and Unit Economics

One of the more cynical comments on the dot-com bubble was the joke “we lose a little money on every customer, but we make it up on volume”.

This refers to the trend for 2000-era companies to focus on rapid scale and user acquisition over sensible monetisation strategy. Grow now, worry about profit later. This approach is justified with three assumptions:

- 1. Economies of scale or new technology increasing margins further down the line.

- 2. Optimism about user lifetime value.

- 3. Reliance on user acquisition gaining momentum in future that will reduce cost.

One or more of these assumptions may be true, but it is a mistake to rely on them without a razor sharp focus on KPIs for acquisition and margins. There needs to be warning signs as early as possible if progress is slow relative to burn rate and runway. The importance of these metrics is highlighted by Finologee CEO Raoul Mulheims: “The fact that you have to have full control of relevant metrics at all times goes without saying … in my opinion the CEO has to be the ‘chief numbers guy’, so he’s able to both challenge every team member and immediately have the right answers for investors, clients and partners.”

Sacrificing margins for growth can also hamstring your ability to innovate and adapt. Having the financial robustness to cover anything from funding a new feature to a complete product pivot can make the difference between life and death for a startup. Nicolas Buck, CEO of SEQVOIA commented: “Our sales cycle can be up to 24 months so there is little room to get it wrong in terms of margins. Also the innovation of tomorrow needs to be funded by the revenue of today.” Timothy Nuy, Executive Director of MyBucks explained their pragmatic approach to profitability from the outset, and how that enabled them to continue developing and adapting: “Our focus when we started the business was to ensure that we were generating profit from the onset. We had a basic business model which we implemented and then built a profitable foundation. This foundation enabled us to raise capital, develop our technology further, and grow the business organically in addition to calculated geographic expansion, and selected acquisitions.“

2. Strategic Agility: Continuous Learning and Adaptation

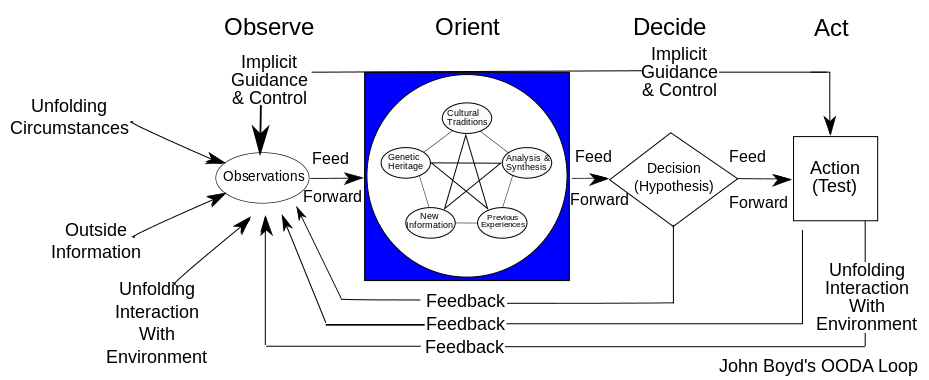

Military strategist and United States Air Force Colonel John Boyd devised a system to define agility in combat operations, referred to as the OODA loop: Observe, Orient, Decide, and Act.

Diagram: Patrick Edwin Moran

This system has been applied to the world of startups for about as long as there have been startups, and is the precursor to much of the logic behind ‘The Lean Startup’ ideology. The loop prescribes that after each ‘action’ the user returns to ‘observation’ to evaluate consequences, and the process begins again.

This approach prevents startups from investing too much time and money into development strategies that ultimately aren’t achieving the desired effect. It is tempting to believe that poor results can be remedied by doubling-down on investment, but often this is an example of the sunk cost fallacy. It’s important to stay humble, and avoid being protective about your concept. Raoul Mulheims offers two key considerations: “First, focus on the product and indeed make sure to challenge your strategy, your features, your pricing … basically all product ingredients at all times. Secondly, don’t always go by the ‘How to Build my Startup’ book: you have to take some shortcuts, make educated guesses, trust your gut feeling, otherwise you’ll be too slow. Challenge your strategy with a few people that you trust either for their knowledge of the industry you’re in or that have a solid background in product building.”

This is particularly relevant to the world of financial technology, where the speed of innovation is not only driven by the multi-directional evolution of technologies, but also rapidly expanding customer expectations and impending regulatory requirements. As mentioned in relation to tracking unit economics, this can make early profitability vital to cover unforeseen costs related to development changes. MyBucks CEO Dave van Niekerk adds to this: “Being a fintech, the environment in which MyBucks operates is extremely fast-paced and dynamic. With new innovative financial technology being released on an almost daily basis and ever changing regulation in its market, We can’t afford to be slow in responding to these conditions. Hence, to remain relevant and competitive, flexibility at MyBucks is core across the board.”

On the other side of the coin, Nicolas Buck warns about the risk of over enthusiastic agility — distracting from the long term goals and product roadmap: “Great technology to be applied to a business model takes time. Flexibility is a word that cuts both ways. It is both necessary and important to keep customers in the loop in terms of product development but the big picture and the road ahead is very much about conviction. So no definitive answer on that one.”

3. Hire the Right People, Treat Them Well, Incentivise Them Correctly

Industry magazine Business Insider curated insights from 28 top CEOs about their hiring practices. Broad themes included looking for natural optimists who will be able stay positive during challenging times, proactive attitudes, and valuing raw materials rather than expertise. Hiring for Fintech brings it’s own set of challenges. What kind of balance do you want to strike between traditional finance expertise and entrepreneurial innovators? Do you want creative risk takers, or critical thinkers who know regulation inside and out?

Passion, not just for the industry, but for the specific project itself is also very high on the list of desirable traits, in fact it’s top of the list for Raoul Mulheims: “The first thing [we look for] is that they really want to work with us. Not just the industry or in any random startup company, but they should have a good idea what they will get into and show some true interest for what we’re doing. The second check we apply is actually a pretty classic one: people we hire have to have a truly solid skillset.”

Dave Van Niekerk describes how their hiring practices ensure the right people are put into the right roles — making the best use of their backgrounds: “We employ “industry mavericks” in our technology and creative and leadership roles, and we place the “conservative thinkers” in our governance, risk and compliance roles. This balance enables us to meet regulatory standards and at the same time be innovative, agile and a catalyst for digital financial inclusion.

Of course, Human Resources isn’t just about hiring, it’s about ensuring your employees are in the most comfortable and productive environment. We already mentioned the two ends of the spectrum found in fintech: Entrepreneurs applying technical innovation to the reinvention of old solutions, and finance veterans who have an intimate knowledge of the sector and the opportunities. Nicolas Buck highlights the need to make sure those groups share knowledge and each understand the problems of the other: “For us as a Regtech in the Funds space — we need to get the mix right — industry professionals and great techies — and we need them to share and work together. I think that is probably the biggest challenge to get the flow of expertise in the different areas of the business moving. What we don’t want is product development to say that the techies don’t understand the funds industry.”

Final Thoughts

Above we have outlined and explained the three most significant considerations for growth, and we did so by leveraging the expertise of local startups. If one point could supercede those three, it is community and mentorship. If you are part of a collaborative ecosystem — including government stakeholders, investors, corporate partners and other startups — you benefit from a wealth of knowledge and wisdom sharing that would take you decades to accrue yourself. They have made the mistakes you can avoid, and they will happily share their successes and advice — much as they have in this article.

Above all of the strengths we benefit from in Luxembourg, the spirit of collaboration is first amongst them. Regardless of the occasion, we can rely on the local support of the fintech ecosystem, and a government that knows financial technology is the future of the country’s primary industry.

“Luxembourg is a great place to develop a business. Incredible things can be done here, simply because the local players, instead of just wanting to grow their own business, want to and are able to collaborate and do something great for the whole country.” — Nasir Zubairi, LHoFT CEO