On the 24th of June we were fortunate enough to host a showcase on Luxembourg’s Payments industry, as a part of our International Showcase series of webinars with Luxembourg For Finance and representatives from across the ecosystem. We’ve transcribed the full talk and Q&A section here.

Antony Martini, Engagement Manager, LHoFT Foundation

Welcome to our second International Showcase, a series of four webinars, today we’re focusing on the Payment Industry in Luxembourg. Our six speakers are the following:

- Chris Hollifield, Fintech development and Fintech advisor at Luxembourg for Finance.

- Thibault De Barsy, Vice Chairman and General Manager of Emerging Payments Association EU (EPA EU).

- Samuele Pinta, Founder and COO of Satispay, a leading Fintech firm from Italy based in Luxembourg.

- Karen O’Sullivan, Head of Innovation, payments, market infrastructures and governance Department at Commission de Surveillance du Secteur Financier (CSSF)

- Natasha Deloge, Deputy Head of Department at Commission de Surveillance du Secteur Financier (CSSF)

On the moderator side, we have our co-host and my colleague Alex Panican, Head of Partnerships and Ecosystem at the LHoFT.

Alex Panican, LHoFT

Thank you so much for the introduction Antony.

We started these financial industry showcases to show to Fintech companies, from outside of Luxembourg, what the financial services and technology ecosystem here is like. Payments technology has always been a big part of the Fintech ecosystem in Luxembourg, so today we bring together a few experts in that field to help explain what Luxembourg is about on the payment side and to answer your questions. As Anthony mentioned, we have the privilege to have Karen and Natasha from the CSSF with us. Thank you so much. They will take your questions during the Q&A.

Chris, let’s start first with you? What’s going on in the payment industry in Luxembourg?

Chris Hollified, LFF

To start off: why are we even talking about payments at all? Why is this important?

One of the big trends at the moment is something that we refer to at Luxembourg for Finance as ‘Amazonisation’. Generally speaking, we think about this in two ways, particularly in the payment sector. Firstly, the development of financial services platforms, primarily digital, which provides a greater range of choices and gradual efficiency to end clients. Secondly, which is particularly important in a payment sense, is the more traditional association that you might come away with the wider Amazonisation form, which is the development of e-commerce. Increasingly, since the beginning of this millennium, we’ve seen huge growth in Payment Services alongside the development of e-commerce.

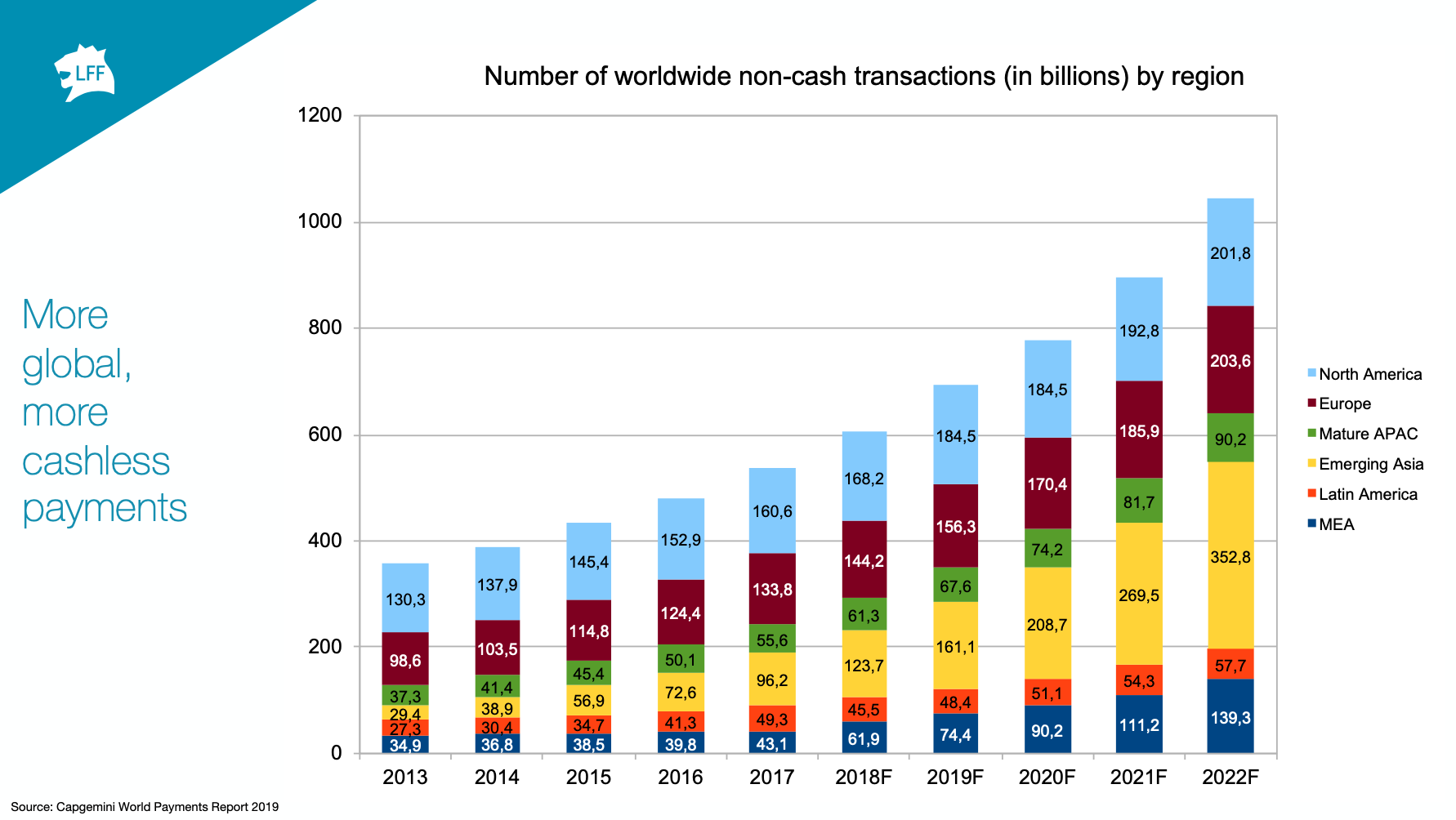

To prove that, here is a slide that I’ve taken from a recent Capgemini report, which shows the colossal ongoing growth of payment services, obviously, very much so in Asia, but also in Europe. Luxembourg has always been at the center of that development in Europe. PayPal, for instance, obtained its banking license in Luxembourg in 2007.

Luxembourg tends to attract big players who are operating B2B in the payment services or in the e-commerce space. Why is that? I’m going to talk about why that is, and what it might mean going forwards.

They’re not coming to Luxembourg because of the domestic market. One of the peculiarities of the situation we live in Europe, in comparison to the rest of the world, is that Luxembourg is a founding member of the European Union. There is free movement of goods, capital, services and people throughout a market of 450 million customers. From a payments perspective, this is unlike Hong Kong, for example, where you have to apply for a variety of licenses if you want to come and cover Southeast Asia, or in the US where you need multiple licences to cover various states. In Europe, if you’re regulated in one particular jurisdiction, you’re able to passport or provide your services throughout the rest of the EU. So that’s a key reason why Luxembourg is as important as it is for payment services.

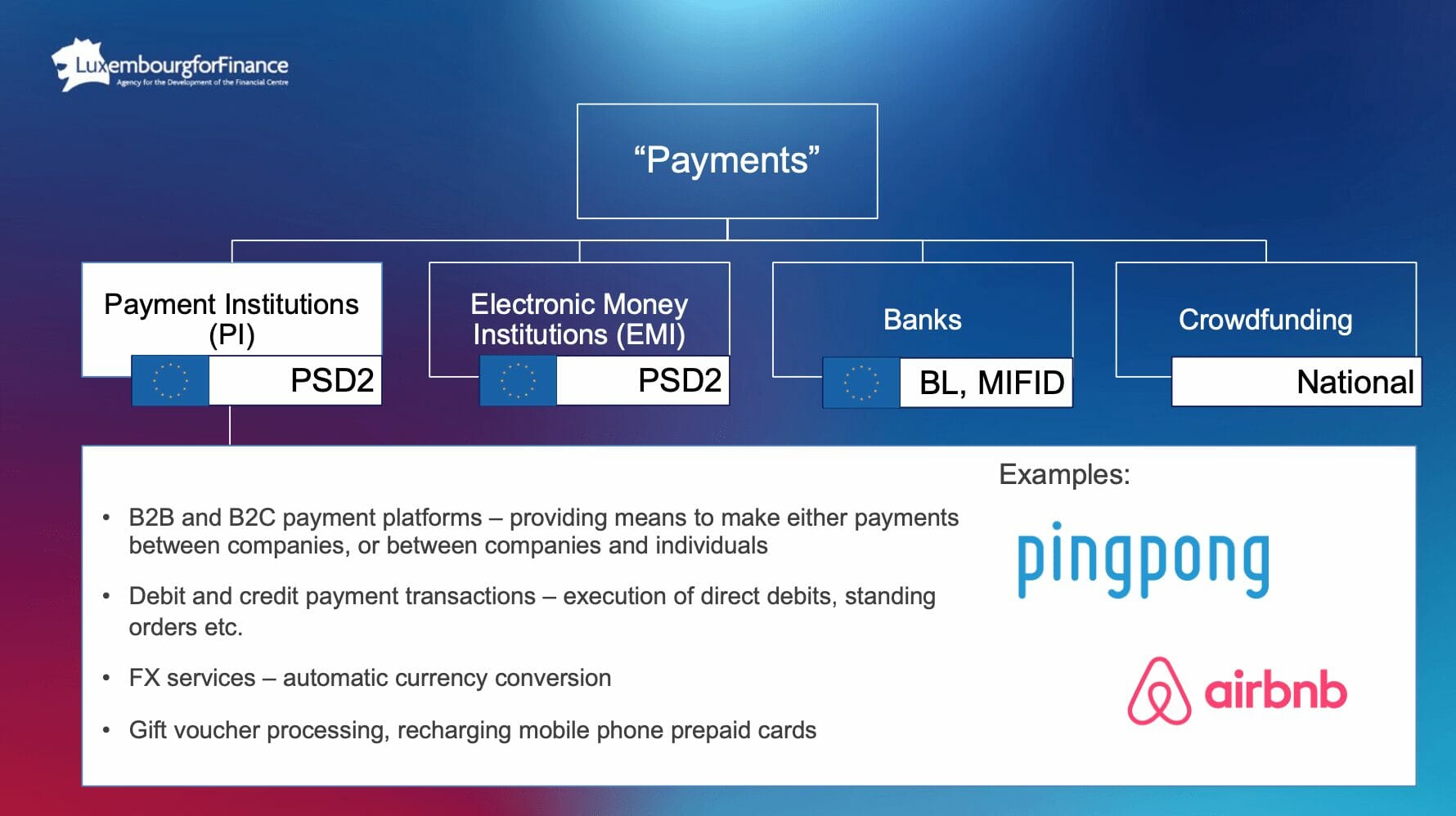

In terms of payment services, for the European context, we can broadly split it into these four different categories. Firstly, we have payments institutions and Electronic Money Institutions (EMI), both licensed under one specific European directive called Payment Services Directive (PSD). Then we have Banks who obviously provide, in addition to a wide range of other services, payment services that are licensed under separate regulatory regimes, including MiFID. And then we have the things that are developing at the liminal edge of payments, crowdfunding for example. The reason why I’m mentioning that specifically, is because there is currently no no European level of legislation on crowdfunding. So it’s something that is not able to be passported across the rest of the EU.

Payments institutions are essentially providing the rails between two accounts, so the cash doesn’t actually sit with you at any point. You’re really just responsible just for the transfer of cash between two servers, between two separate accounts, and there are a number of other additional services you can provide: FX services, prepaid mobile phone, prepaid cards and so on. Electronic Money Institutions (EMI) are essentially where you’re starting to talk about digital wallets. So here, you load these accounts with cash, which is then transferred into e-money which is monetary value that is stored specifically in that fixed ecosystem that you have inside your own company. And then as you’re able to transfer that out in return for goods and services. Then banking obviously, there were wide ranges of services that you can provide to banking. That’s really where you start taking cash deposits and you’re able to provide loans and other banking services. And the reason why I particularly point out just banks is because unlike in say Asian geographies, there is no distinction in Europe between a virtual banking license and a banking license. There is just the universal banking license in Europe. I you apply for that, then you’re able to either provide a buyer for your services virtually or in physical bank.

Finally, to touch on crowdfunding – there is no current EU wide regulatory framework in place, so all crowdfunding platforms in Europe, are dealt with at a national government level and on paper. We’d expect this to change relatively soon; it’s part of the European Commission’s Fintech action plan to develop and create a framework for crowdfunding.

So, with that background in mind, why would companies potentially choose Luxembourg? One of the main reasons is the deep experience we have in these kinds of activities. We have a world-renowned fund center, around 120+ banks from all around the world, 100 insurance firms, and various other things and capital market services. It’s a well-developed financial ecosystem that has been here for since easily the 60s and then really developing in the 80s. We have a wide range of professional services to support your development, ranging from your IT infrastructure, research and development opportunities, legal firms to help you get your licensing and so on.

Finally – andmaybe this is too much direct promotion of the CSSF – but we have a fantastic regulator. This is a multi-lingual regulator, highly experienced in the regulation of cross border financial services, which has been the ‘raison d’être’ of Luxembourg’s financial ecosystem from the beginning.

Alex Panican, LHoFT

Thank you so much, Chris.

Next is Thibault de Barsy, who just launched EPA EU. So Thibault, can you tell us more about it?

Thibault De Barsy, EPA EU

The Emergent Payments Association is 15 years old. It was founded in London, and it has coverage all across the UK, EU and even Asia. In view of Brexit we founded the EPA EU Association in Luxembourg last February. So, we have 150 members in the network based in London, but we already have 12 founding members here in Luxembourg, including very prominent players, such as Visa, Mastercard, and Amazon.

So, what’s the EPA all about? Well, basically three pillars.

We like to facilitate business between our members, and therefore we are organizing a whole suite of events happening in London but we plan to have events in Paris, Amsterdam, Luxembourg and Brussels this year right after the summer.

The second pillar is to provide marketing intelligence and education to our members. Therefore, we have a Payment Academy where our members send their new hires to be educated about payments. And we also organize Hot Topic seminars, which are half day seminars about a particular topic.

And the third pillar is that we have common projects. So we have working groups, which are covering all areas of payments, meaning regulation, technology, international trade, and financial crime. Some of the groups are run from London and we are running two groups from Luxembourg, one on financial crime and another which will aim at producing a white paper describing the EU’s payment landscape, especially the differences from one European country to another. So here we are the EPA EU based in Luxembourg, but covering the whole Europe from here. Thank you so much.

Alex Panican, LHoFT

Is it any particular reason you choose Luxembourg? When Brexit happened, what was your process?

Thibault De Barsy, EPA EU

Well, of course we had to find a location within the EU. The prominent payment players here established here in Luxembourg such as PayPal, Rakuten and Airbnb make perfect neighbours and a core group to start covering Europe to start with. And then of course, our friends from the LHoFT and Luxembourg For Finance were quite instrumental in helping us to settle here.

Alex Panican, LHoFT

So now to introduce the LHoFT, which is a part public, part private foundation. Our goal is not to make money but to help grow the Fintech ecosystem here in Luxembourg, and foster innovation in the financial industry. We are a partnership between the Government of Luxembourg – mainly the Ministry of Finance, Luxembourg for Finance, the Chamber of Commerce – and 20+ private partners.

As you can see, those are the main banks, insurance stakeholders, asset managers… We connect them with innovation, with Fintechs. Today there are 74 Fintechs hosted at the LHoFT and more than 150 members worldwide. Don’t see us as an incubator; see us as a facilitator, because we want to connect you with the financial industry, the regulator, with the different institutions here in Luxembourg.

This is the Fintech map of Luxembourg. As you can see, Payments is already a huge chunk – more than 30% of all Fintechs here. We currently have roughly 220 Fintechs in Luxembourg, generating over half a billion in revenue.

Of those 74 Fintechs, we have six originating from Luxembourg. Most are international companies who have resettled here, and we’re going to hear from Samuele of Satispay who are quite satisfied with that experience. You can also find a huge financial ecosystem with support from public initiatives like the LHoFT, as well as private accelerators, and you’re going to find quite some financing. We also have a huge research and development ecosystem, with university research centers. So there is a full value chain for Fintechs who are coming here to establish and grow their business. That’s what we want.

The last thing I want to point out is that we work with more than 15 other Fintech hubs in Europe, and more than 25 all across the world. So, when you come to Luxembourg, we can make sure that you can work towards Europe, from Portugal to Romania and beyond, easily.

If you have any questions, please reach out to us. We’ll be happy to respond. And now we move on to Samuele from Satispay – can you share your experience with us?

Samuele Pinta, Satispay

I’m glad to be here to share my experience with you all. I’m the co-founder of Satispay, which is a mobile payments solution that can be used by consumers to exchange money or to pay online or offline. The particularity of Satispay is that we are not dependent on traditional credit card or debit card networks, but we are based on debt instruments, and we have more than one 1 million customers.

We were based in London until just over a year ago. We started from Italy, as we are Italian, but we wanted to have a financial app in order to provide our services all over Europe. When Brexit happened, you all know how tough a moment it was. So at the beginning of 2018, we started looking around Europe in order to find a perfect spot for us in order to provide services all over Europe, and Luxembourg was one of our destinations. We came here in July 2018 for three days, and well it was pretty awesome because we had the chance to meet Luxembourg For Finance, then the LHoFT and we got a lot of connections with the people of the Fintech ecosystem or people that would really help us in order to establish our e-money institution. We also met the CSSF, which was interesting because we had the chance to talk directly with them about our business, get their feedback, and our deadlines because Brexit was planned for March at that time. The CSSF was pretty clear with us: they said we cannot guarantee that you can have the license by March, but if you file the application fast enough, and if the quality of the documentation is good, we can try.

When we came home, it didn’t take long to understand that Luxembourg was the perfect spot for us. It didn’t happen in any other country that in three days we had the chance to meet the regulator, get a clear and comprehensive understanding of the situation and our needs in order to get licensed. So we started looking at documentation for the filing, we were already authorized by the FCA, but we had to work a little bit on adapting the documentation for Luxembourg. By October 2018 we had filed for the application to the CSSF and incorporated in Luxembourg, even though we were not obliged to at the time of filing, but we wanted to demonstrate our commitment. We weren’t here just to try to get an authorization. We really wanted to be here.

From October to February we stayed close to the CSSF, clarifying all the points regarding the application. Finally, in mid-March, we got the license and by the end of March, we could migrate all our customers from London without any disruption to the services at all. We also relocated physically from London to Luxembourg thanks to the LHoFT. We stayed there a little bit since they are offering these offices as part of their offer which is super interesting because you can start there, you don’t need to look at real estate or other co-working spaces. You have time to do those kinds of things, and in the meantime, you can start and do your job.

We have the Italian holding company, which takes on all the IT developments and so on, but all the regulated part of the business is managed here in Luxembourg, and we are happy to be here. I really think that one of the most interesting parts of Luxembourg is this ecosystem. Luxembourg is quite small, and we had this joke when we were here in July 2018 that every meeting was within like 15 minute’s walk, so it’s quite small, but it’s super international and plenty of knowledge and it is super easy to share knowledge or to be in contact with other parts of the Fintech or the financial industry. And I think this is one of the most interesting parts of Luxembourg. And we are super happy to have chosen Luxembourg.

Alex Panican, LHoFT

Thank you Samuele. Did you encounter any difficulty or anything unexpected in this process? Can you share any advice for entrepreneurs looking to do something in Luxembourg on the payments side?

Samuele Pinta, Satispay

I think everyone with an interest in the industry is here to help you, because Luxembourg is mainly focsued on financial services. So I think you need to be very serious, and you need to be committed. We wanted to demonstrate that we really want to be here, so we incorporated the company from the beginning, and so on, because if you are able to provide your commitment, then I think on the other side, everyone can understand that and will want to help in order to increase the financial capacity of Luxembourg.

Alex Panican, LHoFT

Thank you Samuele.

Karen, thank you again for being with us. We already have questions regarding the FCA and Brexit, so how close is the Luxembourg financial regulator with the UK? Let’s start with the politics and then we’ll get back to business.

Karen O’Sullivan, CSSF

We are in touch with all of the regulators across Europe, in constant contact with them. And the FCA is no different in that. So we have always been in contact with them. And then at the moment with Brexit, different discussions are still continuing. I think we’ve received quite a lot of applications to set up business in Luxembourg because of Brexit, and it was something that was also coordinated with, depending on the market, with ESMA, to make sure that wasn’t a race to the bottom and that the level of regulation was maintained and respected.

Alex Panican, LHoFT

Of course. One question we have quite often, and that Samuele mentioned, is about companies that are regulated by FCA, looking to get a license in Luxembourg. Is the process faster because they’re already regulated?

Karen O’Sullivan, CSSF

If a company already has a license in the UK, it could help them because they’ve already had the experience of going through a licensing process. So maybe parts of an application are already prepared, or documents that exist that may just need to be tailored to the specificities of the business that we would like to launch in Luxembourg. But the fact that they have a UK license does not mean that this is a fast track to Luxembourg. Any entity will need to go through that same licensing procedure, will need to submit the same documents, will need the same level of detail in those documents, and we will be doing the same review on the contents of the documents. Quite often what we can see is a previous experience means that people are more prepared to answer the type of questions that we would ask, and have prepared the type of information that they would need to provide.

Alex Panican, LHoFT

Is there any specific difference between the two applications?

Karen O’Sullivan, CSSF

I suppose, yes, any activities may be similar, but I think we need to see what is going to be planned in Luxembourg, the substance of the number of employees, the offices that are planned in Luxembourg, or what activities will be provided to the Luxembourg market. So it’s really taking the general information that may be there, and we need to see how it can be specific to the company.

Alex Panican, LHoFT

Perfect. Quick question from Jerome, what are the main trends, challenges for the new entrants in the payment industry in Europe and maybe in Luxembourg to start with? What is the advice you will give them?

Karen O’Sullivan, CSSF

I think for us it’s very important that people are very clear about the activities that they want to provide, very clear as to the license that they are looking to obtain. We do have something in our Luxembourg law that if you have a license, and if you haven’t started the activities within the year, the license is taken away from you. So companies need to be careful.

Alex Panican, LHoFT

I know that’s quite unique because many of our Fintechs say that they are surprised after the first meeting with you because you ask me about their business plan. I don’t know if it’s unique to the CSSF, but you’re also looking to make sure that the business is viable and there is a real business behind the application.

Karen O’Sullivan, CSSF

I wouldn’t say we like to say whether it’s viable, because we don’t give any guarantee or comfort or sign off of the viability of the project. But we do look to make sure that this plan activities in Luxembourg, that the activities make sense, and fall within the requirements.

It is part of the EPA guidelines for application plans and a business plan needs to be submitted. So I don’t think we’re unique in asking for it. But it’s something that we would ask for, in advance of any meeting so that we can understand what the company is about.

Alex Panican, LHoFT

Entrepreneurs often ask us about your process. Do you have any advice on the specifics that they should be careful about?

Karen O’Sullivan, CSSF

For us, it’s really the substance of the people that are expected to be put in place. And we need to make sure that the central administration of the entity is in Luxembourg. So the first to have a central administration, Luxembourg, that means you need the appropriate staff, the appropriate staff at different levels and different kinds of expertise, depending again on the activities, and that the Luxembourg market is being served in those activities. That’s very important for us that we need to make sure a plan is in place and is sufficiently solid if you’d like for us to move forward. Also that the group itself has the financial capacity to assist an entity in the startup phase. We know that in the payment sector, in the Fintech sector, it is entities that are in the startup phase, there is more finance required and funds. So if an entity is looking for licenses, financial requirements need to be respected. And we need to make sure that the group as a whole, depending on where it’s going, is in a position to financially support the company because the last thing we want, either for us or for the market, itself is lots of entities obtaining licenses and then financially not being able to meet the requirements within the first few months of their operations.

Alex Panican, LHoFT

I will get back to you, Karen, in a little while. It’s amazing to have the CSSF with us, it’s quite unique. Fintechs don’t often speak with their regulator.

Now a question from David Lozano. He has a question for Samuele, and maybe also Karen, or Chris can jump in.

David Lozano, H2o Fintech

My question relates to moving to Luxembourg because of Brexit; I think it’s not yet confirmed that your UK license won’t be valid for the rest of Europe?

Samuele Pinta, Satispay

Yes. Well, you are right. It’s still to be defined what’s gonna happen but you know, when you are a company, especially in the startup phase, you need some clear certainty about what’s going on. Otherwise, it becomes too difficult for everything you’re gonna do. If you have to employ people, they are going to ask you what’s going to happen with Brexit, and you can’t not have an answer. And so, we tried to wait and see in 2018, but ultimately we decided to move.

Also because we were still not offering our services in the UK. The other option was to create another subsidiary in Luxembourg, keep both companies, but we said okay, it’s the EU market for us, now it’s more interesting, so let’s move the company there, starting from beginning with a more solid base. If one day we’ll have to get back to London, if the freedom of passport services will be available, we will be able to use it from Luxembourg or otherwise we’ll have to establish a new subsidiary and so on. But at least now we are sure that we can provide services all over Europe without any uncertainty over our head.

Alex Panican, LHoFT

Maybe somebody wants to add to that. Is Brexit for real?

Chris Hollified, LFF

Brexit is definitely for real because we’re discussing the future relationship, Brexit has already happened – we are in a transition period. So yes at the end of the day, you’re taking a bet, and one way or the other. And it’s really a question of how you want to hedge that.

I will point out that in large numbers, financial institutions have already taken the step of setting up European subsidiaries when they were based in London. I would take that as a sign that these guys consider it to be a big deal.

Alex Panican, LHoFT

Coming back to licensing, Karen, how long does it take? Imagine that these companies will lose passports rights to Europe. If they apply in Luxembourg how long it will take to get the payment or EMI licence usually?

Karen O’Sullivan, CSSF

It really depends on the file. It depends on the complexity and the nature of the activities. It depends on how prepared the company is to submit their file. And as summarized I would say “the level of quality of the file”. So we do have entities that get a license within six months, we do have others where it might be closer to 18 months. So I think it’s really dependent on what the company is trying to do, how well explained it is in the file. And also the level of interaction or collectiveness on behalf of the entity. As Samuele said, there’s a lot of back and forth questions. So it depends on how quickly and how thorough we can get those answers back as well. So there’s no kind of definitive time but it’s, I suppose on the shorter end, it could be five to six months, or anything up to a number of years.

Alex Panican, LHoFT

We are almost in July and I guess you guys are quite busy also. So, if I (as a Fintech) cannot make it by the end of the year to get a license, do you have any advice for me?

Karen O’Sullivan, CSSF

I think at this stage, from where we are, you would need to be considering an intern backup solution. So maybe an agent or some other type of arrangement with an existing company that has a license, pending the company obtaining the license early next year. But at this stage, it’s very hard for us to or nearly impossible to guarantee any more licenses for files that we have not yet received or for people that we have not met before the end of the year.

Alex Panican, LHoFT

Quick question for Thibault. Can you share the top three innovations you witness in the payment ecosystem in Luxembourg or in Europe?

Thibault De Barsy, EPA EU

Let’s take the Europe angle. I think that what you can see is that you really have some countries which are advanced in some defined fields.

For example, if you look at the Nordic countries, they are the kings of instant payments. The proportion of instant payments within those countries is just huge. So that’s the best practice to follow.

When you look at account to account solutions, which are now going to be even further facilitated by PSDII and open banking, you should look at the Netherlands with iDEAL and Germany with SOFORT, which is now purchased by Klarna. Why? Because those guys came with account to account solutions even before PSDII, so they definitely have some advance there.

When you look at P2P payments, you should look at Italy with players such as Jiffy. They have made instant payment very easy and very popular within the Italian markets.

So that’s what’s fantastic about Europe is that you have excellent players everywhere. And even if you don’t look at Fintech specifically, but you could also look at the corporate payments in the B2B payments, you can see that traditional banks are doing a pretty good job there to facilitate payments and make them instantaneous for very large amounts and for cross border payments between continents. So that’s very encouraging.

Alex Panican, LHoFT

Anything you want to add Karen or Natasha? I mean you must see many different business models and so many different innovations.

Natasha Deloge, CSSF

We do not have any favourites, but the business models become more and more challenging. With the kind of platforms that are presented, that offer different kinds of financial services, there are certainly business models where not only a payment institution license but also another potential financial sector license may be applicable and where we have to find some solutions on how to regulate this.

Alex Panican, LHoFT

Coming back to us innovation. We have a lot of questions, and one main field that is raised almost every day is crowdfunding. There are so many different crowdfunding platforms that are looking to launch. I don’t know if Luxembourg is the right place for that. Maybe Chris, you disagree with this. Karen, what’s your input on crowdfunding? What’s the regulation regarding crowdfunding? And are we going to see more? Chris, you can jump in, if you wish, afterwards.

Karen O’Sullivan, CSSF

From a pure regulation perspective, there isn’t a harmonized EU approach at the moment. It’s more national regimes. So we’ve decided not to have our own national regime. We are following the European approach. There is a draft directive, which we were following. So I think from a pure regulation perspective, we would wait for an European movement, and then we would follow that movement and not look for a national regime.

Chris Hollified, LFF

I think that that makes complete sense. By its very own definition, crowdfunding wants to pull in capital from a wide variety of different sources, and it just doesn’t make sense if you’re basing it purely on a national base regime, particularly in a country like Luxembourg. However, the potential for crowdfunding when you have a potential base of 450 million investors is kind of mind blowing. So it’s really about waiting for the Europeans legislation to come out so that we know the overall framework that we’re operating in the European context. And then from there, I think that would be the real catalyst for developments in that field.

Alex Panican, LHoFT

Before speaking about cryptos and ICOs, and that’s another subject that we have many questions about, we have a question about substance. And I think it comes back to what Karen you mentioned, so as Chris and Samuele. You have to be serious. You have to put your team here in Luxembourg.

So on that topic, a question from Arnaud Wenger:

Arnaud Wenger, iPayLinks

I’m Arnaud from iPayLinks in Luxembourg. So I have a question about the substance, because technically our main clients are in China. And we are here to set up everything and to follow the full Luxembourgish and European legislation. It’s very important for me to have compliance based here.

What I’ve noticed is, with Chinese clients, having an all Chinese team that has a better understanding and access to certain tools that we cannot access here has advantages. So is it enough to have someone here in Luxembourg to supervise and control what the Chinese team are doing, or do we need to move the whole team here?

Karen O’Sullivan, CSSF

There are certain key tasks that are to be performed by the company which cannot be outsourced elsewhere, and many tasks in their day to day business that can be outsourced elsewhere in the group or externally, but everything that takes place right there is under the direct responsibility of the local entity.

So I think in your case, if some of the compliance type tasks are outsourced to a group company or an affiliate in China, which is closer to the market, it’s not a problem as such. But clearly the ultimate responsibility for anything that’s client related remains in Luxembourg. We would look to make sure that you can demonstrate that the team in Luxembourg is fully aware of what’s being done, is fully responsible for what’s being done and is aware and involved in key decision making. So for instance, onboarding of any new clients, has to be approved in Luxembourg, particularly if it’s resolving different operational kind of hiccups or whatever, that’s being dealt with by a Chinese company because it’s closest to the market, it’s not a problem as long as again, you are aware of it. So, yes, there can be outsourcing or working with different companies, but the ultimate responsibility has to be clear. And it’s very important that the notion of central administration is preserved. And that means appropriate for an adequate number of staff in Luxembourg, to be able to assume that responsibility.

Arnaud Wenger, iPayLinks

That’s very important for me to know that I can keep my teams for example, in China because it’s much easier as they can speak directly Chinese with the clients and we can monitor what they are doing. So it’s not just simply to rely on them, but also to control them and that it is very important for me to not have to move all the team because it’s so important to be close to the business.

Alex Panican, LHoFT

And now a quick question on licensing from Sergey.

Sergey

My question is as a startup before to see the end of the whole process going with the authority, is it possible to apply for a simple agreement very narrowly limited in payments in order to start doing business sooner?

Karen O’Sullivan, CSSF

No, we don’t have different levels of license. Ultimately a license is a license. However, there is an article in our law where, if you are below certain thresholds in volume on an annual basis, you could start operations without obtaining a license. So in that case, it would be possible to possibly start your operations while applying for your license. But it’s really depending on the volumes and if you exceed those volumes, your operations would need to be on hold or suspended until the license is applied. So it’s the same license, but in particular, where you could start if you’re a real startup.

Alex Panican, LHoFT

Regarding post Brexit, how do you see the perspective for Fintechs from India coming to Europe? Do you see any kind of collaboration in the future?

Thibault De Barsy, EPA EU

Well, very good question. For example, a member of the London Association is FSS technologies, which is a huge player in India. And they have chosen initially London as their European headquarters, and now as they want to expand towards Europe, and they are definitely a very good example. And obviously, India has a lot of technologies in terms of electronic money, so they know very well how it works. I feel they would be very welcome as a new player and certainly within the EPA EU.

Alex Panican, LHoFT

Changing topic a little, a question from Kunal Patel.

Kunal Patel, 1E

Real-time payments have a huge focus now with a lot of the card schemes and other companies. I had a conversation with Visa Europe here in the UK about that, and they’re scaling up pretty quickly around real time, and it would be good to get a perspective from a Luxembourg point of view, from an European point of view on real-time payments, given, of course, all the regulation pieces coming into play now, like new ISO standards and so on.

Karen O’Sullivan, CSSF

For instant payments, there is discussion on the local market and time to get ready. So it’s not something that we’re following up with, it’s not something that we’re pushing actively from a regulatory perspective. We would accommodate the banks and are encouraged to help the banks. We would like to actually try to kind of position themselves in those developments. But there are different discussions going on to try and push it forward.

Kunal Patel, 1E

I think that’s the challenge. If you think about the UK, there’s an organization called Pay UK, they’re going through a whole kind of look at infrastructure to support all the emerging payment initiatives that are taking place here, especially, of course, then that sets the standard across Europe and the rest of the world as well. So, I think that’s where I’m seeing a lot of focus right now, in that sort of next phase of how payments are going to be managed on new rails using new guidelines and infrastructure and standards and so on and so forth. So, there’s actually quite a lot of stuff going on here but we’re talking possibly you know three to five years out from now really once all that has been kind of laid forth really but interesting journey nonetheless.

Alex Panican, LHoFT

I’m just gonna give the mic quickly to Samuele. As you work in this industry, anything you wish to add?

Samuele Pinta, Satispay

In terms of instant payment in Europe, there’s still a lot of work to do. The main problem is, as per PSDII is the harmonization between the standards, between banks. The banks need to speak the same language and it will take a bit of time. The UK is a bit ahead of us also with the PSDII because they started with Open Banking a little bit before but we are getting there. For others, as a Fintech company, I have to say we’re still a bit struggling in order to leverage on this kind of instrument, because of this the harmonization between banks and approach and so on. It will take a little bit of time that we’re getting there.

Alex Panican, LHoFT

Thank you to everybody. Thank you for the listeners, please drop us an email and connect with us because as I said Luxembourg is quite open and we’ll be happy to be a facilitator for you. Thank you again to our panellists and wish you all a great day ahead.