Until medical breakthroughs become widely available – consider the logistical challenges associated with vaccine candidates currently undergoing development – COVID-19 and the ensuing, profound societal limitations will continue to impose a long-term adaptation of business models and policies.

Last month, I highlighted data points and initiatives in Luxembourg which underline the emergence of a new paradigm that combines technological transformation with societal aspirations. These local developments should be understood as part of a larger dynamic in global markets, wherein ESG criteria and impact investing are becoming the norm all the while major tech companies offering “COVID-proof” services have seen their valuations soar.

Figure 1: comparison of the Dow Jones Industrial Average to Amazon shares, 1-year performance

Setting aside (valid) concerns around the oligopolistic tendencies of Big Tech, there are undeniable benefits to being able to order goods online during a pandemic, processing payments and other financial transactions remotely and securely, or to remain in touch with friends and coworkers via online messaging and videoconferencing. These services are here to stay, posing a formidable challenge to many brick-and-mortar stores, but also opportunities for growth via the integration of physical and e-commerce.

On the policy end of things, across the board, governments have set aside previously accepted thresholds for indebtedness in order to stem the simultaneous demand and supply shock created by the pandemic and create a favorable framework for economic activity in a post-COVID world. Most recently, the U.S. Federal Reserve announced a subtle yet impactful revision to its consensus statement, favoring the maximization of employment over controlling inflation in the medium term.

While the massive fiscal and monetary policy response to COVID-19 sets the stage for economic recovery, the qualitative parameters of this recovery will be set by a confluence of civil society preferences and private sector investment. Reflecting on the confluence of technological change and development goals, the co-chairs of the UN’s Task Force of Digital Financing of the SDGs recently reflected on the “nexus between digitalization, finance and the SDGs” and write that “digitalization amplifies the potential for the financial system to better serve the interests of people, whose money it manages, and whose collective interest is expressed by the SDGs”. The report emphasizes not only technological advances per se, but rather a technologically enabled transformation at the service of a citizen-centric financial system:

Figure 2: schematic from “People’s Money” August 2020 UN task force report

It should be noted that the concept of a citizen-centric financial system implies, at least to some degree, a decentralization of the financial system such as heralded by the blockchain movement. As noted in my June blog post on the topic, citing LHoFT partner Deloitte’s 2020 Blockchain Survey, one “key takeaway [is] that leaders […] now see the [the technology] as integral to organizational innovation”.

Technology investment for global impact

The tremendous potential for positive societal impact via investments in technology and specifically into digital finance / Fintech is perhaps most evident in the developing world, as I outlined back in May. This sentiment is shared and the issue is further explored by one of the UN task force’s members, Governor of the Central Bank of Nigeria Patrick Njoroge, in an op-Ed available via Project Syndicate. As Dr. Njoroge writes, “There are already useful models of such disruption. Africa – especially my country, Kenya – has led the way in embracing financial technology, beginning with mobile money. Kenya’s M-Pesa – a mobile phone-based money-transfer, payments, and micro-financing service – has been a powerful force for expanding financial inclusion. Since 2006, the share of Kenya’s population with access to financial services has surged from 26% to more than 82%.”

Looking beyond the local impact of fintech in Kenya, Dr. Njoroge goes on to describe his institution’s proactive approach to fostering a viable fintech ecosystem, notably by partnering with Singapore’s Monetary Authority as announced last year. This joint initiative, which one hopes will be fruitful, is a great example of the sort of global collaboration that is called for in order to reap the full benefits of technological advances with a view on societal impact.

On a more micro and hands-on level, the role of fund managers and venture capitalists in particular should not be overlooked when considering the confluence of tech and impact investment. A great example of this emerging investment “vertical” is the $500m global venture fund Flourish. A top-level consideration for the fund is “whether [investee] technology advances financial health and economic resilience”, as discussed by Managing Partner Emmalyn Shaw during a far-ranging interview available via Soundcloud and Spotify. She describes a trajectory of personal and career development which led her to leverage her “hard skills” in finance and technology in order to increasingly focus on impact investment. In-line with the broader trend towards ESG considerations in asset management, the growth and successes of Flourish and other funds with an impact angle will continue to cement the economic viability of “extra-financial” considerations, and the necessity to incorporate a “touch for tech” with development goals.

Succeeding after a reshuffle

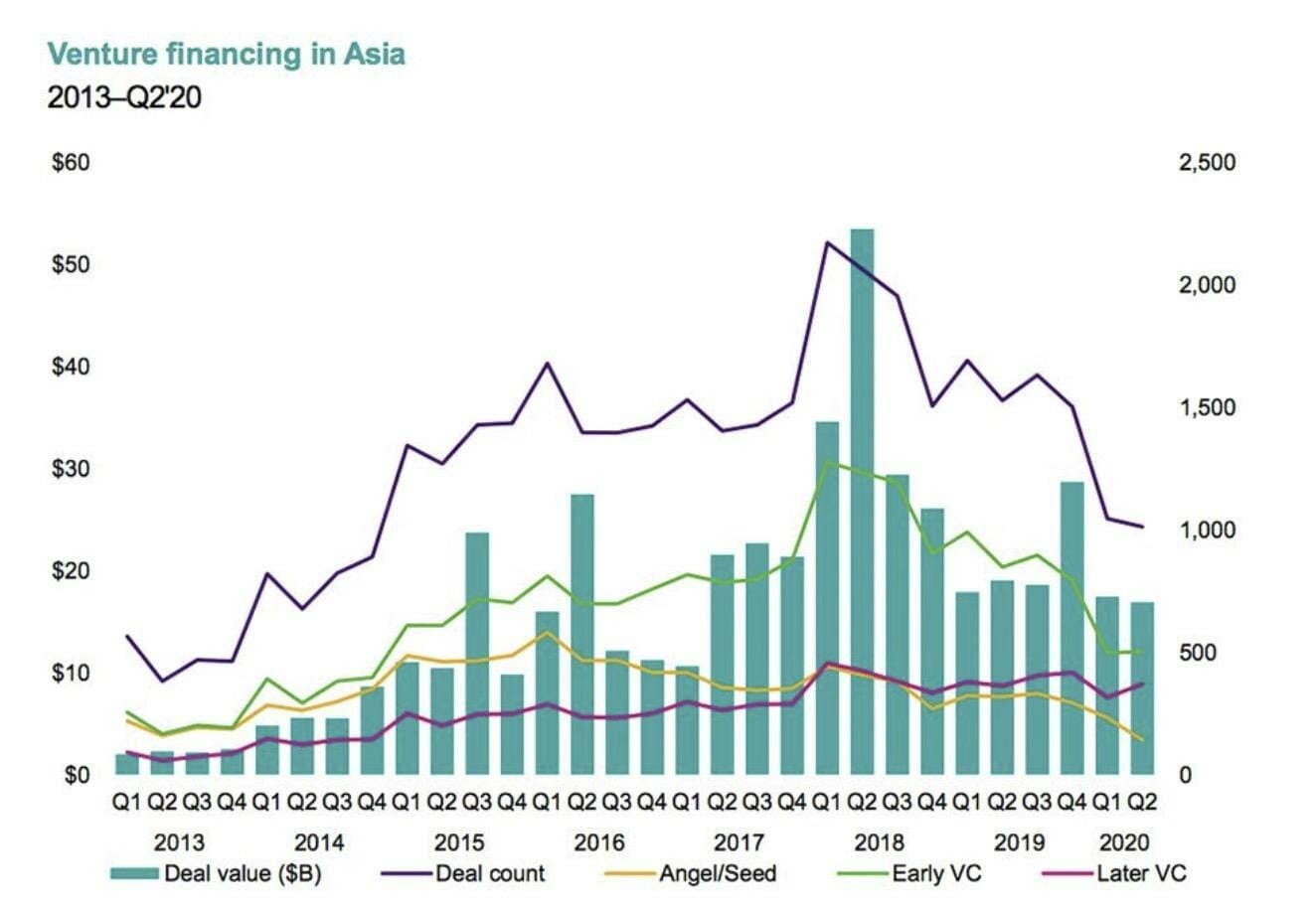

While market opportunities abound for tech and fintech enterprises, major economic crises present with particular risks and uncertainties for early-stage ventures. This is reflected in the significant drop in early-stage financings in Fintech in Q2 2020, as investors took a step back to reevaluate their strategies and portfolio investments. Consultancy.asia provides valuable insights into the evolution of the VC scene in Asia, with investments in China looking poised to pick up again.

Figure 3: VC funding is stabilizing across Asia. Source: consultancy.asia

However, in the face of continued macroeconomic uncertainty, it is reasonable to expect that the preference for later-stage and well capitalized startups will continue, leading to some difficulty for startups at the seed and early stages. Regional differences will also continue to play a role, and may necessitate regionally adapted funding mechanisms. In Europe, the EIF is poised to continue playing an important role in catalyzing VC funding, and more public investment schemes could see the day in the near term. Additional public sector investment would serve as a recognition of the strategic importance of the (fin)tech startup ecosystem for regional competitiveness, financial inclusion and societal impact.

At LHoFT, we are emboldened in our mission by the tangible, positive impact that Fintech is making to the post-crisis recovery and to the overarching goals of development and inclusive finance. We are committed to helping our members succeed via a proactive dialogue with our industry and public sector partners, collaboration on value-added projects and the generation of industry insights.

Fintechs looking for funding in Luxembourg are referred to this comprehensive write-up by LHoFT associate Şebnem Elif Kocaoğlu Ulbrich, which lists notable private sector actors and currently available public sources of funding.

Author: Jérôme Verony – LHoFT Research and Strategy Associate