On the 15th of May we were fortunate enough to host Vikram Haksar and Yan Carrière-Swallow of the IMF, as a part of our International Leadership Perspectives series of talks. The recording is available to watch on our Youtube channel, and the slides may be downloaded here, and we’ve also transcribed the full talk and Q&A section here.

Nasir Zubairi, CEO of the LHoFT

Thank you all for attending this webinar today. We’re very proud and pleased to have Vikram Haksar and Yan Carrière-Swallow from the IMF with us, live from Washington, who are going to give a talk on the economics and implications of data in the financial services arena on a more macro scale. The talk should last around 20 to 25 minutes, so we should have ample time for Q&A. If you just drop your questions into the chat, we’ll then bring you on live to ask the question directly once we finished.

Let me give you a little bit of background about Vikram and Yan.

Vikram Haksar is an Assistant Director in the IMF’s Strategy Policy and Review department. In this role, he currently leads work on finance and technology, macro-financial analysis, and policies for assessing and addressing financial stability risk. He has been a lead author of the IMF’s main papers on fintech, and most recently, The Bali Fintech Agenda. Prior to this he managed review work on global surveillance, G20 prospects, and spillover analysis. Vikram was earlier the IMF’s mission chief for Brazil during the ‘currency wars’ and led the IMF team that set-up the $70 billion Flexible Credit Line agreement with Mexico in 2009 in the aftermath of the Lehman failure. He has worked on emerging economies in Asia––including Thailand during the Asian crisis––and Eastern Europe and was the Fund’s resident representative in the Philippines. Vikram received his Ph.D. from Cornell University.

Yan Carrière-Swallow is an economist in the Macro Financial unit of the IMF’s Strategy, Policy and Review Department. His research interests span various topics in international macroeconomics, with a focus on emerging markets and their policies. Prior to joining the IMF in 2012, he was an economist at the Central Bank of Chile in Santiago.

Gentlemen, welcome. I will now hand over to you. Thank you for being here.

Yan Carrière-Swallow, Economist, Macro-Financial Analysis – Financial Services, IMF

Well, thank you very much, Nasir, and good evening to everyone. Thanks Nasir for giving us the chance to share this work with you. And I’d like to thank everyone for joining us on your Friday evening to discuss this fascinating topic with us.

So the title of the talk is “The Economics and Implications of Data : An Integrated Perspective” and I’ll try to make clear why we emphasize that point in the work that we’ve done.

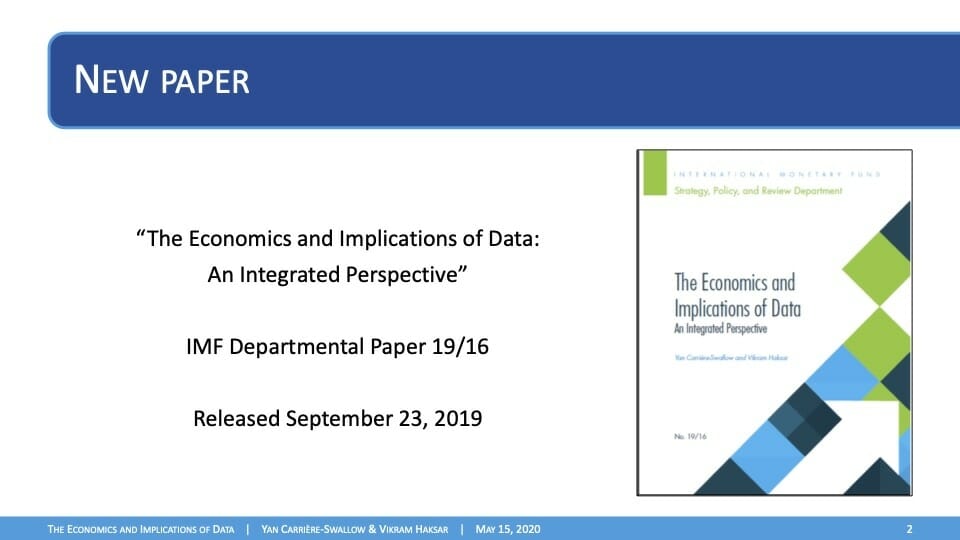

The economics of data is a topic that Vikram and I have been working on for the better part of the year, we’ve written this paper about the topic which you can find online. This talk will be based on the paper. It’ll be a quick overview of the main points, the main messages, but if by all means, if something doesn’t get resolved in the Q&A that you’re itching to find out, feel free to download the paper and take a look.

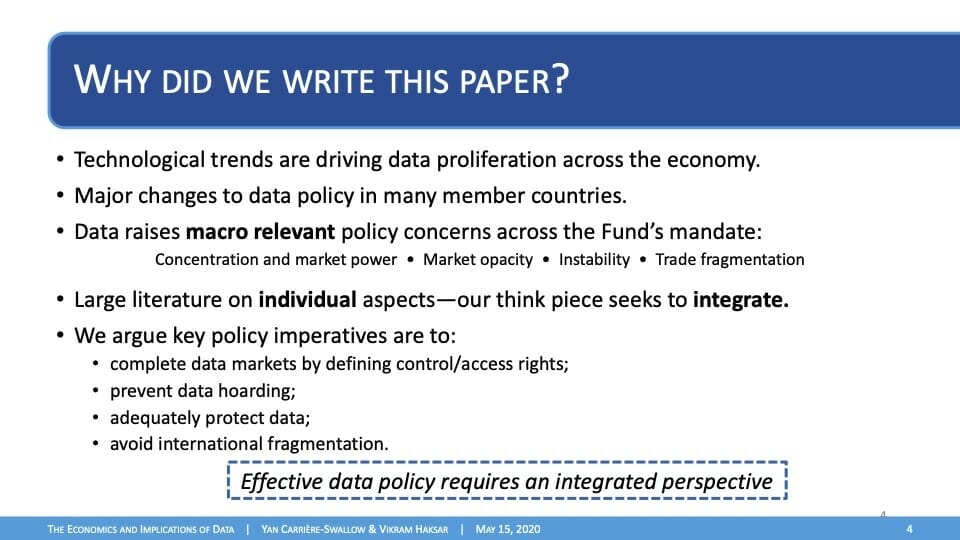

So why did we write this paper now?

So we see a confluence of several trends. The falling costs and improvements in analytics are driving the proliferation of data across the economy, and in all sectors of the economy. We’re seeing discussions of data policies across our membership, with major changes having already been made. We’re seeing reforms to consumer protection, open banking regulations, as well as global data localization laws. So we saw a need to understand conceptually, what all of this means for the broader economy. And as we’ll explain what we find in the work there’s a lot of arguments for why data has many economic functions and implications that raise macro relevant policy concerns right across the IMF mandate.

There’s been a veritable flurry of academic activity on how data-rich economies might function differently than an analog economy. But when we look at these contributions in the literature, usually to keep things analytically tractable, these papers treat each question in a narrow sense, individually. And we saw value in writing a think-piece that would seek to integrate all of these different approaches and materials. We fear that thinking about data policy through the lens of one objective in isolation may mitigate one problem, while inadvertently causing others to pop up unexpectedly. So this piece that we wrote is about identifying the building blocks for thinking about these questions, identifying the main trade-offs that are involved, and putting our fingers on the open questions in data policy, rather than providing solutions or answers. The issues are complex. It’s early in the profession’s engagement with this topic, and our message is that we need to think about these issues carefully.

“Does the accumulation of data deliver economies of scale? Does it give you economies of scope across different lines of business? Is data a compliment or a substitute to your other inputs such as labor or capital?

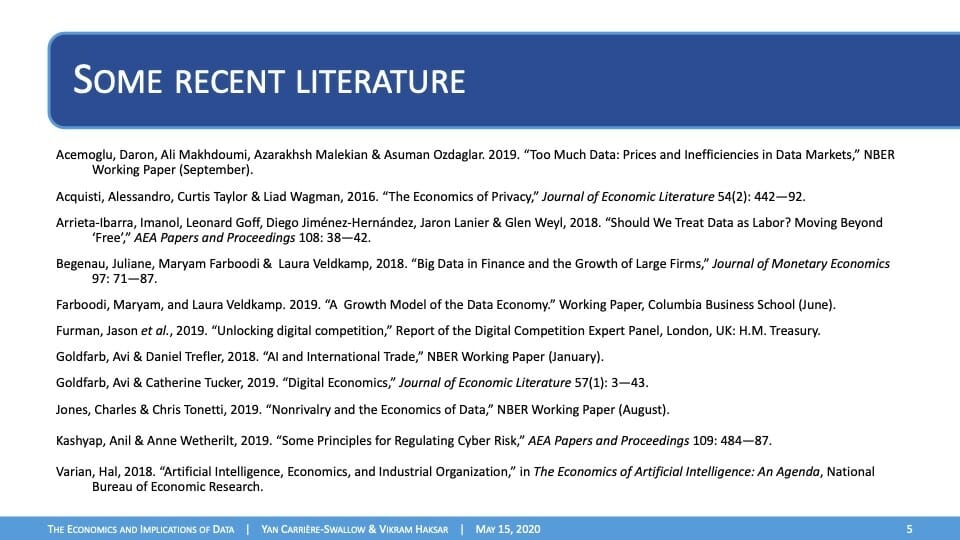

We’ve provided this list of snapshots of some of the more recent papers that we found popping up in the literature as we were working on our piece. For those of you who have studied macroeconomics, or who are active in the field, you’ll recognize many of the names here that are really top-notch academic macroeconomists who are engaging on this question of ‘what does the macroeconomy look like when you introduce a data-rich environment?’ What about when our old models stop working? What are the new policy questions that need to be addressed to avoid getting bad outcomes?

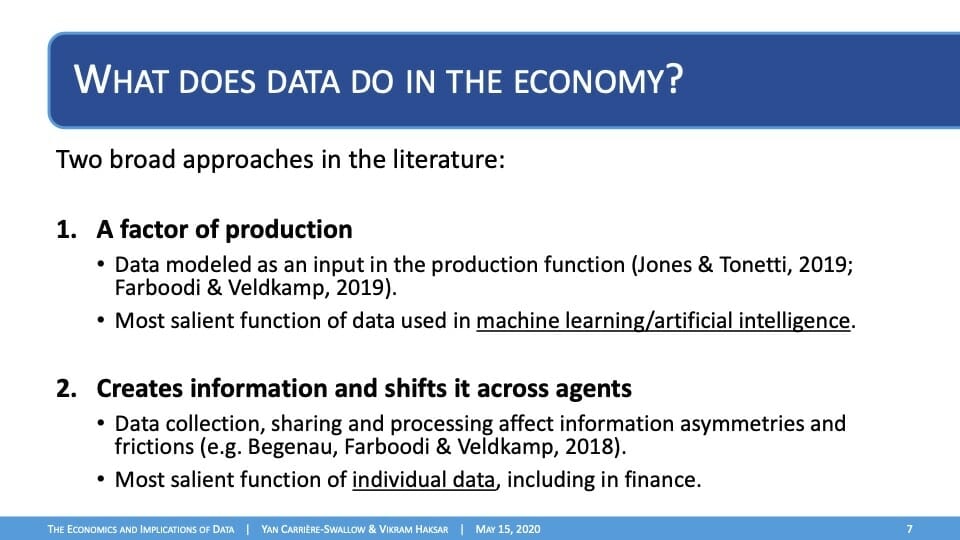

You can group these papers into two broad approaches for modeling data in the economy:

The first thing you find is a more macroeconomic perspective. It emphasizes the data’s role as an input in the production function. So this is an intuitive way of thinking about using data in artificial intelligence or machine learning algorithms to produce a good or service. Now, of course, the devil is in the details in these models, in the sense that the functional form that you choose to write down your function determines a lot of the input equilibrium outcomes that you get from the models. The key questions are going to be things like does the accumulation of data deliver economies of scale? Does it give you economies of scope across different lines of business? Is data a compliment or a substitute to your other inputs such as labor or capital? A lot of people in the literature have strong views about these questions. But it’s important to note that a lot of these questions are open at this point. What we’re finding is an incipient empirical literature that’s starting to dig into the data to start answering and guiding and disciplining this theory so that we can narrow down our understanding of these questions.

The second approach that you find in the literature is more microeconomic. And that emphasizes that when you create data or you trade data, what you do is you create and shift information across economic agents in the economy. And this is the approach being taken in much of the finance literature, where the production and trading of data about borrowers shifts information asymmetries and affects their access to credit, ultimately.

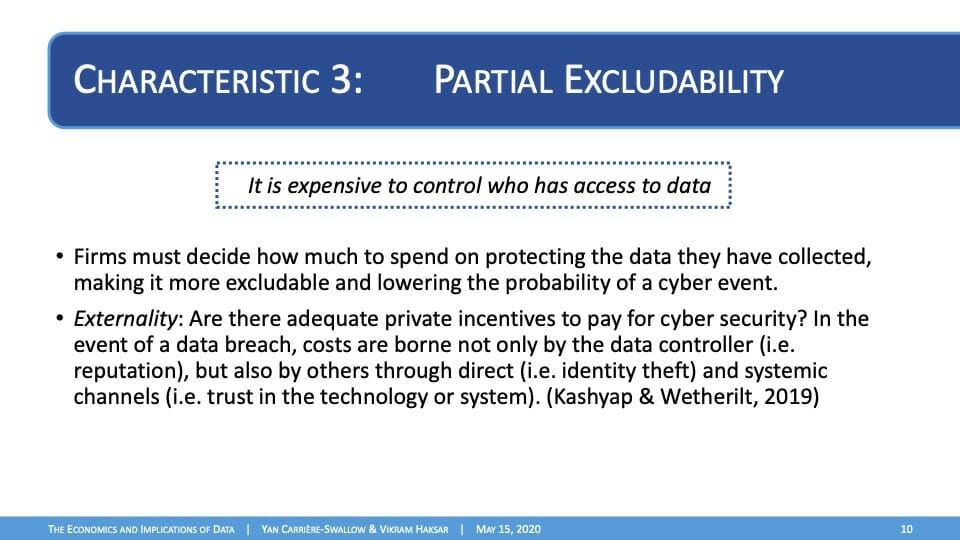

Once you put data into models, it has three key economic characteristics that give it interesting properties that make it unlike other inputs that we’ve thought about before. These can lead to market failures, and they can form the case for policy interventions in the data economy.

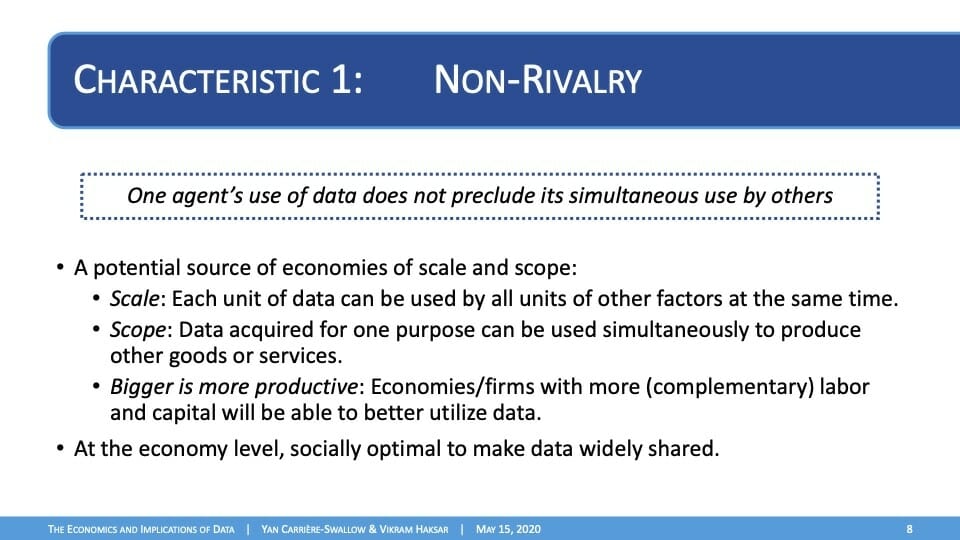

The first of these characteristics is that data is non-rival. So when agents use data it doesn’t stop other agents from using that same data at the same time. This makes data quite unlike other inputs like oil. We hear a lot of the time that data is the new oil. In some ways, yes, but in this respect no, it’s not. When one person uses oil, someone else can’t use it. That’s not the case for data. And an important benefit that can flow from this non-rivalry characteristic is that you can get increasing returns to data, both in scale and in scope. And so the intuition here is that when you add an additional unit of data, when you collect an additional unit of data, that extra data can be used by all units, all other inputs in the production function, not just the marginal unit. So this turns a lot of the main conclusions in the economic growth literature – on how you get growth from accumulating capital, for instance – on their heads.

These economies of scale can apply within a firm, across many firms, and across borders. Many implications flow from that. One of them is that making data widely available tends to allow society to do more with the data, to get more out of it, get more production out of it. A key question is will the data be made available. And here I think an important insight is that private incentives of the people who are collecting the data may lead them to hoard it and stop it from being shared. And there a lot of the benefits from non-rivalry do not accrue. So, because of data’s non-rivalry, a central focus, the first thing that data policy has to set up is to establish rules for who will have access to data and who won’t have access to data.

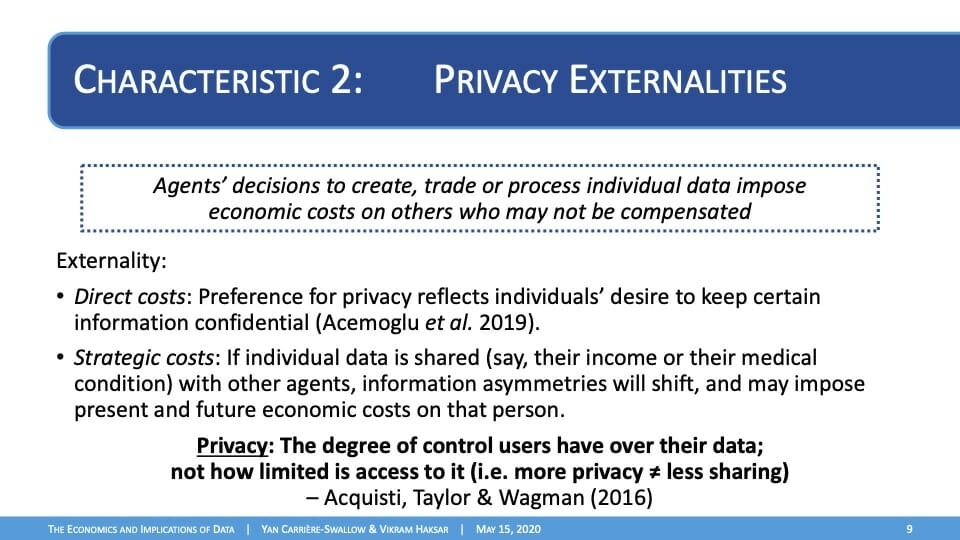

The second interesting characteristic that data has in these models is that it causes privacy externalities to emerge. Okay, so why do we frame privacy this way? When agents make decisions about whether to collect trade or process data, they impose economic costs on other people who are not compensated or who may not even be aware that that decision has been taken. So think about a social media user who shares information about one of their friends on a social network, or the social network itself, selling on one of its users’ information to an interested third party. So an important insight here is that privacy, as we understand it, is not really about mandating less data sharing, less data access, but rather, it’s about granting control to individuals over the data that affects them.

The third characteristic that we pick up from the literature is that because data is kept on interconnected networks, making it excludable is expensive. So investing in cybersecurity is a decision that firms have to make about how excludable they want to make the data they’ve acquired, and there’s an externality lurking here as well, in the sense that the private incentives to make data excludable to protect it may not fully account for the harm to public trust and to the broader system that can result when an individual data set is breached.

What does all this mean for macroeconomics and macroeconomic outcomes? Let me run through a few of the main implications.

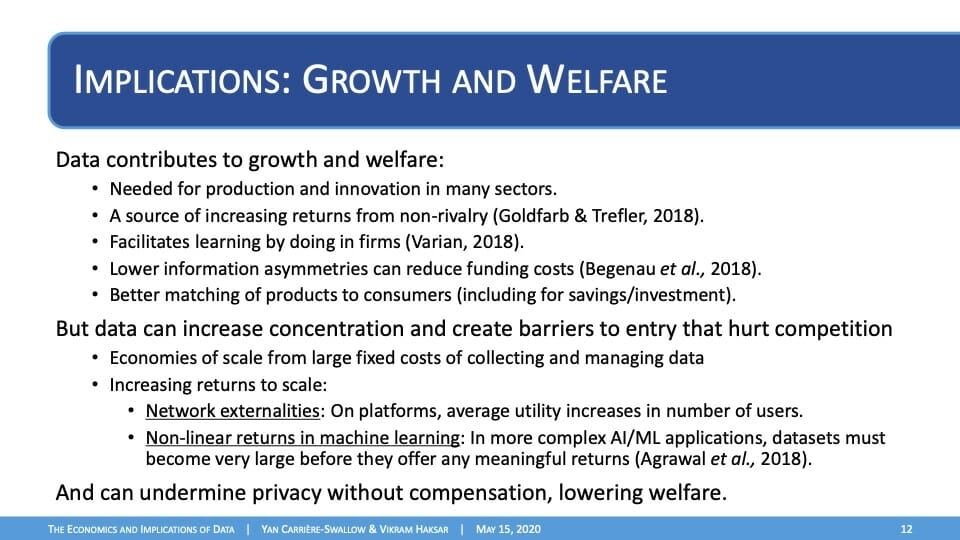

The first set of implications has to do with a data-rich environment having an impact on growth and welfare. Several channels have been proposed for why this might be the case. Data accumulation can allow for more efficient production and can allow for innovation. And it can do these things with increasing returns to scale, which allows you to potentially boost the rate of potential growth. It can be used to improve allocative efficiency in markets, certain types of markets in particular. And it can enable the development of new, more customized goods and services. But the side of the relationship here isn’t necessarily clear. Data accumulation can also form barriers to entry that can hurt competition. These can stem from large fixed costs, or also from network externalities that favor the winner takes all dynamics in data-rich sectors. And of course, data proliferation of data can itself undermine individual privacy, and this can lower welfare directly.

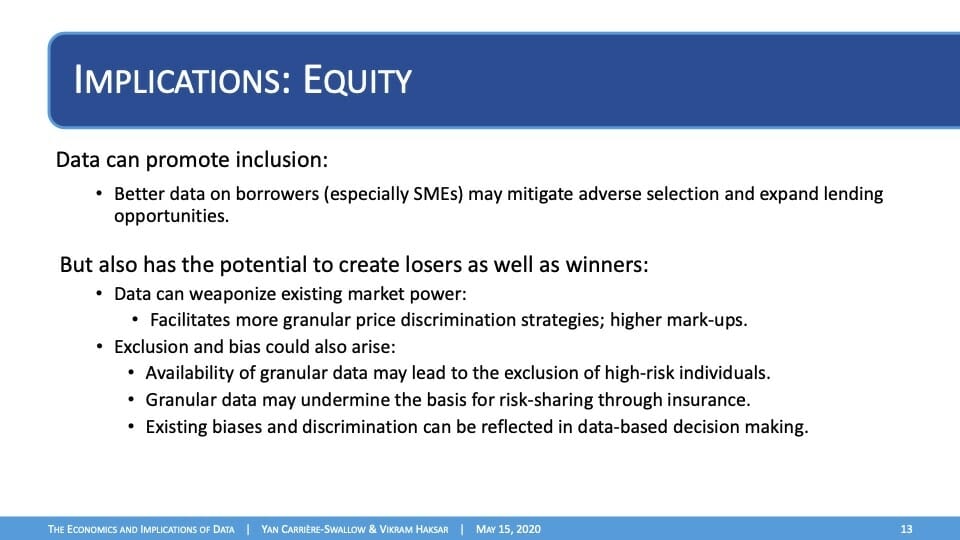

A second set of implications are for equity. What’s received a lot of attention recently, and rightly so, is how data proliferation can promote inclusion by mitigating adverse selection problems that plague small and medium enterprises, and more vulnerable households when they participate. In traditional financial markets, this has received a lot of theoretical and quantitative attention in the literature and I think, has caught the eye of many policymakers, and rightly so. But one of the things that we mentioned in the paper is that data accumulation can also create losers as well as winners. And so for instance, if you give a monopolist granular data about their clients, about their preferences, about their income, their ability to pay, they can weaponize their market power through price discrimination strategies, and therefore charge higher markups and higher profits. Data can also lead to the exclusion of some high-risk individuals, and potentially in the limit where you have a sort of absolute data-rich environment if we think it could potentially undermine the risk-sharing function of insurance.

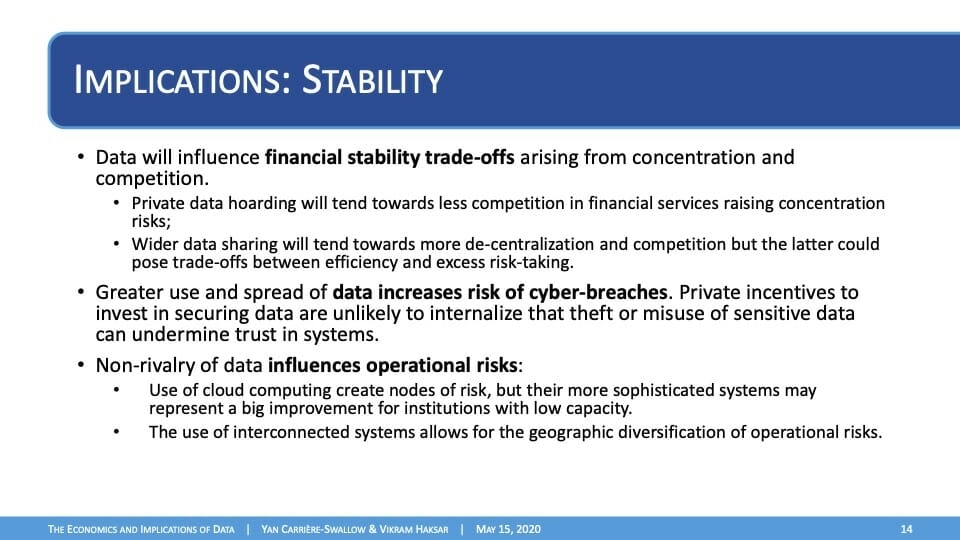

A final set of implications are for financial stability. And here we see two kinds of broad buckets of channels. One argument is that by affecting the market structure and market power in the financial sector, data will influence financial stability trade-offs between concentration and competition, which is a set of trade-offs that’s been studied quite extensively for several years. Introducing a data-rich environment you might think would have an incidence on where you sit on that trade-off, but a second set of channels is also important. Since there may be inadequate incentives to secure data from cyberattacks, heavier use of data-dependent systems, particularly in finance, may increase the risks in some cases, or at least shift them onto centralized service providers, which raises new sets of issues that regulators and supervisors need to deal with.

I now hand over to Vikram, who will say a few words on data policies.

Vikram Haksar, Assistant Director, Macro-Financial Analysis – Financial Services, IMF

Thank you very much. And thank you again to all of our colleagues and friends who are on the call and listening to us on your Friday evening, hopefully with a pleasant beverage in hand. So let me just wrap up this presentation by talking a little bit about the policy implications and a little bit about data policy frameworks.

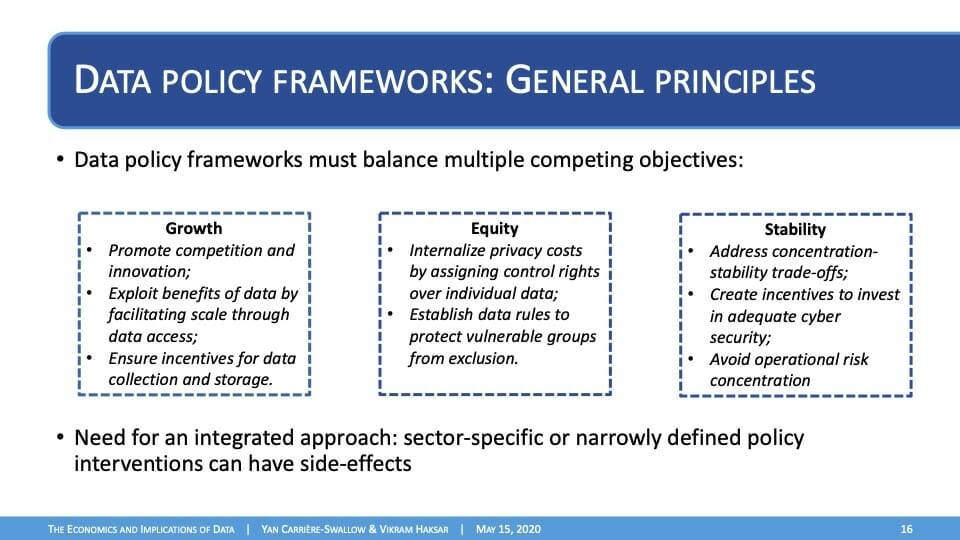

Our basic view is that just as the proliferation of data across all sectors of the economy has implications for macro outcomes, so also do the policies that determine how data can be collected, shared, processed, and protected. And there are many examples of the data policy frameworks that already extend: we have privacy laws, increasingly we have open data regulations. There’s a large trend towards data localization requirements. And of course, we’ve had long-standing consumer protection measures.

“We need data policy frameworks that balance multiple competing objectives – growth, equity, and stability.”

One insight that we come away with at the end of all of this work, and I think as Yan has nicely laid out for us to think about, is that these issues are all interconnected and integrated. And that when you think from a data policy framework, we need data policy frameworks that balance multiple competing objectives – growth, equity, and stability – objectives that different policymakers may have a focus on. In our view, this creates a complex set of trade-offs arising from these interactions. And so our main takeaway is in our view, that data policy requires an integrated approach. We see a need for policymakers to bring the many agencies who have a stake in these topics to the table so that multiple trade-offs can be considered together. Our concern is that handling data policies in sector-specific silos could have side effects.

Two simple examples: Consider, for example, if we were to strengthen privacy laws, which is an important critical objective from a consumer protection point of perspective, how does that impact the ability of firms to compete and innovate? And would this have an impact on lowering growth? Another example would be let’s say that we were to implement data localization requirements, which many countries are doing from a national security standpoint. And in that context that we might ask, in a world with excessive data localization, will fellows be able to achieve the scale of data sets needed to tackle physical AI problems? Think about in Luxembourg if you had a company that wanted to start up a self-driving facility. And if the only data that was available was on the residents to Luxembourg, that would be very difficult to get the scale to train the cars self-driving algorithm. If you want to do that you want to have data to the whole European system to all the individual driving information, the whole European system on the United States. I think this is a side effect we were quite concerned about.

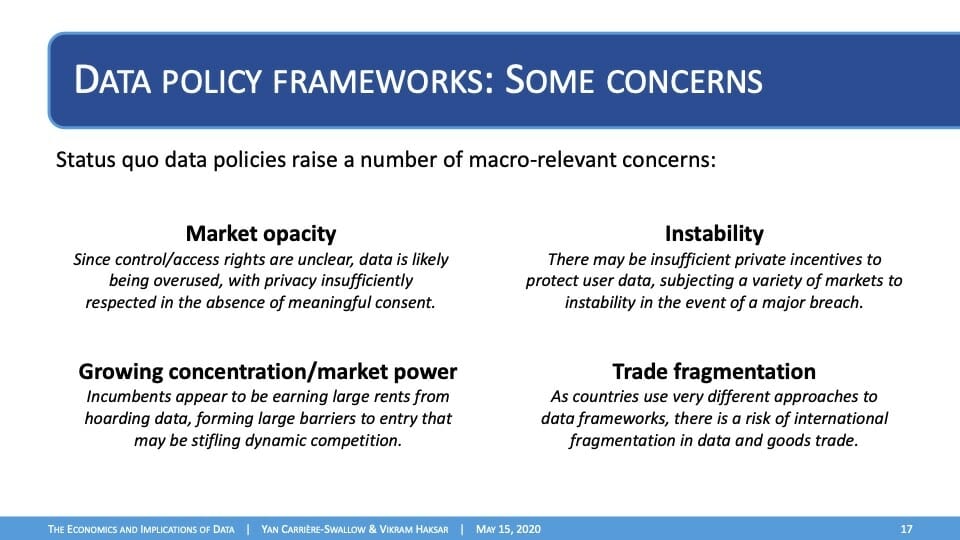

So as Yan has mentioned right at the beginning, we see a prima facie case that data is raising for macro relevant concerns. And this is why we, at the IMF, are quite interested in the topic as well. The first is on market opacity. So a clear place to start is to clarify the rules of the digital economy.

Our concern is that the market for data is too opaque suddenly from a consumer perspective. Control and access rights over data are unclear at best. And this means, in our view, that data is likely being over-utilized, at least from the perspective of the individual consumer, and that privacy is not sufficiently being respected.

The other macro concern is competition. We seem to have a growing concentration of data with sectors with incumbents building market power and extracting rents through data hoarding, holding on to data sets. As Yan laid out, were they to be more widely shared with both increased competition and by the mechanism of sharing allow for people to exploit the non-rival nature of data to innovate and lift productivity growth in the whole economy.

The third macro concern that we have is the prospect for raising instability. And you know, just to be very clear here, we recognize that all corporations and financial institutions have a very large stake in protecting that data. And in protecting that consumer’s data. There’s no question. Cyber Security is a major cost point and there’s a huge incentive for all institutions to protect their data. I think the subtlety that Yan was explaining was that while each institution may have this incentive from the system perspective, from the perspective of the authority, who’s concerned about the overall system, would individual entities take into account the damage to system-wide trust that would take place, would there be breaches in any one part of the system given the nature of cybersecurity?

We’re concerned that we’re seeing the potential for rising instability not because of any individual action, but just because the world is getting more interconnected and the potential for these kinds of breaches to occur is increasing, as we all know very well. So tackling this systemic externality that is that people talk about is a challenge to monitor and regulate. And finally, let me close by saying that from the IMF’s perspective, countries are approaching data very differently. And this is something that we’ll be thinking a lot about, and we are going to be looking at doing additional work on. Our concern is that we may be heading towards fragmentation. Now, certainly all countries are sovereign, they have the right to be interested and looking after their concerns and prerogatives. Our only suggestion is that in thinking about the individual needs that countries face, we would argue that having some international discussion about whether there’s scope to have common minimum standards and approaches to minimize unnecessary fragmentation would be extremely important. Without this, there’s a risk that with fragmentation, with the example I gave you about self-driving cars, you could see significantly reduced gains from trade in data. This could also hamper trade in goods and services that use data as an input. And I would think that this is an issue which would be quite relevant, including in a small financial model as well, but in the large financial center, like Luxembourg. So with that, let me stop here. Thank you again, very much for your attention.

Q & A Session

Nasir Zubairi, CEO of the LHoFT

Gentlemen, thank you very much for that interesting presentation. We have several questions that have arisen. So what I will try to do is to allow those people to ask those questions directly because I always find me talking on behalf of people is unnecessary. So I’m going to go first in order here. Dan Feaheny, I think you can ask your question.

Dan Feaheny, Principal, Feeney Ventures Ltd

Hi, gents. Nice to hear that. It’s great to hear the research at the macro level. And looking at other studies. I’ve spent a lot of time and continue to spend time in open banking going to open finance. And there are two issues: one is the issue of identity. So identity, should it be federated or self-sovereign? Should it be controlled by governments or by banks? And if I can ask quickly Nasir, the other question that I put up there was compare the frameworks of the US and the UK so far. US market lead, UK kind of looking at regulation, and, you know, controlling it from the open banking implementation entity. So the US had an industry consortium called FDX. And then the UK, quite controlled getting the CMA9, you know, asking politely for data sharing from the banks and having all these third party providers. I’ll stop there. Thank you.

Yan Carrière-Swallow, Economist, Macro-Financial Analysis – Financial Services, IMF

We’ve been doing a bit more work on open banking. We didn’t have a lot to say in this first paper, but it’s certainly one of the main applications that we think are very relevant. Open banking regulations, about mandating data portability and interoperability within the financial sector, I think has potentially large implications for the traditional banking model in which a bank would essentially be able to monopolize to some extent, the information that they have over their clients, precluding some degree of competition. And as we study that less conceptually more operationally, we come across these important issues like the one you raise, how should identity be managed and implemented? And I think I think Vikram has some views on this based on the Indian experience that I think could be useful for this discussion.

Vikram Haksar, Assistant Director, Macro-Financial Analysis – Financial Services, IMF

Thanks, Yan. I think I would say two things, one on the open banking part. So some of a lot of the discussion we’ve had, including with members of the high-level advisory group to the IMF is that the ecosystem is now quite diverse and the ecosystem in finance and technology is very diverse. And regulation is still focused around what you might call the traditional intermediaries, banks, you know, in the last decades, increasingly non-banks, but the value of actors in this space has become very diverse. From a sort of principles-based approach, there’s a strong argument to be made for data portability and interoperability of systems, for the reasons that we layout in the paper. This is something that is pro-competitive and allows us to use the non-rival nature of data to achieve better things. But there is a need at the same time, in my view, to have a level playing field out here, which is that it’s not just the case that incumbents who are already existing in operating the space should be providing access to their systems and access to API’s and their systems. But it should be something that is two ways. So that other entrance into this space also should be sharing data and providing access to information. My guess is that, especially as we get into thinking about some of the larger technology players entering into financial services, defining what is the space of information that is relevant from a finance perspective, that should be shared, it’s going to be a key challenge. And then defining what is the perimeter of how far sharing and how far into existing systems, the new entrance or existing incumbents are allowed to penetrate? I mentioned those of your important questions. On your question of digital ID I think that’s key. This is something we’ve begun to think about. We haven’t done a lot of work on the topic ourselves. We’ve begun to look at it in the context of international competitive experience of approaches to open banking. We have been looking at the approach in places like the UK versus say the approach in Australia versus places like Singapore and India, regardless of whatever the case may be, digital ID – to our minds – is key.

We do need to have some ability to have an identity, which can be verified and attached to financial transactions in this digital economy. I would just say two things will be in their perspective, which I don’t think I’m going to fully answer your question. We’ll give you some views at least. One is that operation operationalizing digital identity, I think is a huge challenge. How do you make it come about especially in countries with very large populations or the level of income or the level of state capacity might be lower? And the India experience I think shows that self-sovereign identity has huge advantages out here. In terms of you have a large population that may not have the ability to provide all the necessary documentation. The sense of a piece of the digital identities is, I think, quite important, actually being able to achieve scale and a relatively short period of time. I think the other issue that comes up and which is an interesting example from the India case is the tension between digital identity that is managed and controlled by a state agency, that high level of Federation, the tension between that and privacy. And you know, we’ve had cases in India already, which has been heard where the government at various points in time was seeking to increase the ambit of transactions that require the digital identity. The Aadhaar, for example, to be used for a plane ticket, you want to buy a cell phone, you’d have to provide your Aadhaar Identity Card identity number, and that there was a public interest litigation with the Supreme Court ruled against the government saying that it was not permissible to use digital identity so widely.

So in the India stack, which we think is an interesting example to how you might manage and balance concerns on identity, privacy, while also getting access to the use of the data. The India stack approach is to conceptualize as an entity as a data fiduciary that will manage your identity and your data on your behalf, and be as a kind of a circuit breaker that could address the multiple concerns there might be, which I think in principle sounds very good. Now, the question that we don’t have clarity into yet and we’re still exploring is how this would be implemented, but from a sort of conceptual perspective certainly sounds like I think it’s sort of a third party neutral arbiter whose incentives are aligned more with the incentive of the individual would make a lot of sense.

Nasir Zubairi, CEO of the LHoFT

Okay, fantastic. There’s another question that’s come in from Naja; please, go ahead.

Najia Belbal, Senior Program Manager, Nomura

Thanks a lot for this interesting presentation. I just want to have your view on the fact that when it comes to the data, we all have been taught that it’s really interesting to have data and to exploit them. But with this Covid19 crisis, we have understood that we face some kind of uncertainty. By that I mean not enough data to understand what’s going on, a lot of ambiguity, because even when we have data, we don’t know how to interpret them. And you know, a higher probability to fail or to get errors from there. So how can we overcome such a situation from a data point of view?

Vikram Haksar, Assistant Director, Macro-Financial Analysis – Financial Services, IMF

“How do you square the need to collect data and information which has a huge public interest aspect to it with the fact that individuals don’t want to be tracked and monitored by the state?”

Naja, thank you. I think that’s a fantastic question. And it’s something that Yan and I have been, in this dark new world of COVID, starting to think about. The way we’ve been thinking about it is that clear to the many views about how we proceed with managing the pandemic and containing it, and what the final steady state is going to be. But it’s varied, and many policy pieces will have to be sorted out, there’s a lot of uncertainty about all this.

I would venture to say that one part that is quite clear is that efficient contact tracing is key to containment and prevention of the spread of the pandemic. And by that meaning that being able to keep tabs on who has gotten the disease, who’s infected and who they’re coming into contact with so that we can quarantine people and impose measures to ensure the reproduction factor begins to drop. And the approaches to contact tracing are fascinating in the East Asian context in China, where the state has faced the trade-off between the social need and the individual right to privacy, there is I think very heavily in favor of the social need. And then the approach that the authorities have taken is a very strong approach by contact tracing is mandatory. And individuals are on cell phone penetration is extremely high, smartphone penetration is extremely high. So you have a situation where because of that both high penetration and the app and the and the mandatory requirement of use of contact tracing applications that use geolocation. It has been quite possible for the state in these contexts to have a fairly efficient mechanism for keeping tabs of the dynamics of the contagion and being able to implement policies of containment.

I understand that this is a big debate in Europe where, of course Europe with GDPR, you know, has had an approach which places a very heavy emphasis on individual rights privacy. I think it’s something that we can all relate to and understand that this is an important issue. So, we see that this is a big challenge. How do you square the need to collect data and information which has a huge public interest aspect to it with the fact that individuals don’t want to be tracked and monitored by the state? So we were wondering, again, this is an easy thing to conceptualize. But it’s a question that we want. One has to think about how to make these things operational.

We were wondering whether the approach being taken in India, again with the notion of the data fiduciary might be a way out. As you can imagine a situation where data in a social context where there’s a high premium on data privacy, where this kind of contact tracing related data was collected in a manner that was fairly autonomous and centralized in an agency may be centralized with keys that were not known unless there was actually evidence that contact had taken place. And then there was some protocol that the keys will be revealed only to a third-party neutral agency that will not be associated with other aspects of the instruments of the state. Some mechanism where there’s a firewall, a kind of a cutout in between the individual and the state with all of its other aspects, some in-between kind of third party neutral centralized body that would not see individual data until there was contact. So that’s something that we wonder, we were very interested to hear if other people have views on this, actually, but it’s something that we’ve been thinking about as maybe a potential solution leveraging some of the insights from the India stack approach to actually solving a real pressing problem.

Nasir Zubairi, CEO of the LHoFT

Thank you very much. Thank you for your question. And next up, we have a question from Susanne Schartz

Susanne Schartz, Chief Operating Officer, Seqvoia

This is a very interesting presentation. Thank you. I’m coming from a much more practical level. In what we see today, I think that most of the data is being collected for specific means. So I’m collecting data to use it to then sell more to my clients or somebody else. You know, you’re coming from a much higher level approach of collecting data, protecting data, and how can we ensure access to all of this? How do you think that awareness could be raised at both industry and national levels to say data needs to be looked at in a much more general way, which will lead to a massive increase of the usages that you can make of data.

Yan Carrière-Swallow, Economist, Macro-Financial Analysis – Financial Services, IMF

“There’s a disconnect between how much people say they value their personal data, and what their actions imply.”

I think there’s interesting questions of how much people value their own privacy and their own data. It is a really interesting, fascinating field of study. And the answers are remarkably difficult to tease out of observational data. There’s this paradox of privacy that comes that’s well documented in the literature where if you ask someone, how much do you value your privacy people will always say that they place a very high importance on their privacy. They would be willing to pay a lot of money to protect their privacy, because it’s super important to them. However, if you look at their actions in the economy, most users are willing to trade that away, to sign a ‘terms and conditions’ that releases very important aspects of their data in exchange for a minimal online service a lot of the time. And so there’s a disconnect between how much people say they value their personal data, and what their actions imply.

I think one of the ways you can square that it’s not the only way, but one of the theories that we see as being quite important is this problem of opacity. Are people even aware of what is going on, what data is being traded? I think one of one aspect of your question was to ask, you know, how can we increase awareness, both among the public and among policymakers, and I think a first step, and a step that’s been, you know, effectively taken in Europe already, but in the United States I think is a little bit earlier on, is just to make sure that people are aware of the transactions that are taking place. One of the ways you can do that is by setting rules. I think when you buy an “Alexa” enabled device in your house, what are the rules? What are they allowed to listen to? What are they not allowed to listen to in your conversations? What are they allowed to do with that data that they collect? Can they sell it on to somebody else? Etc. There’s a hodgepodge of legal precedent and rules that are out there. But I think for the consumer, it ends up being that you have maybe some intuition, but you don’t know. Having clarity is a first step to making people aware of what’s going on and then having a discussion about how we make change it.

Vikram Haksar, Assistant Director, Macro-Financial Analysis – Financial Services, IMF

Let me just add a couple of quick points. I think the claim that we make in our work is that (this is economist’s talk so bear with me) we claim that the data market is not complete, and is not complete, because there are pockets of information, not everybody has the same access to information. It’s not a level playing field, and therefore I don’t know what my data is worth. I don’t know what I’m signing away. So I think Yan has laid out the case that, you know, we feel I think the steps are beginning to be taken. And just resonating with me is your question about the practical aspects of it. And if I may shoot a little bit from the hip out here, think about something like GDPR. We’re now in response to that requirement, data providers are asking us to check a lot of boxes as to whether we accept cookies, whether we are willing to sign away, a lot of things will be a lot of fine print, etc. And to get a service and it’s very difficult for consumers to effectively give this consent. Are you well understanding what you’re consenting to? For example, if you’re going to be doing mortgage finance, the United States has a well-established body of regulation and jurisprudence about what the consumer rights are, how you should inform the consumer about the risks that taking you know, and during there’s a long list of frequently asked questions. So that requires some coordination, cooperation to figure out what is the basic minimum information required to make people understand what’s going on, and to have a standard that can then be implemented uniformly across different sectors and frankly, potentially across different countries as well. It may not be the same fit for every country, but maybe at least having some common approach, some common minimal approach would be helpful.

Nasir Zubairi, CEO of the LHoFT

There’s quite a few questions. We’re not going to have time for them all, but I need to follow up on this one because we’ve had this discussion a little bit before. Is data an asset? If it’s an asset, how do we protect it as should we be protecting it as an asset? How should we value it? You know, we’ve talked about the way that the advertising industry, etc. I was wondering if you’ve thought a little bit more about this and what happened and your thoughts on this for the audience.

Yan Carrière-Swallow, Economist, Macro-Financial Analysis – Financial Services, IMF

“I think it’s quite misleading to equate the transaction prices that we’re seeing currently as being a true reflection of the full value of data.”

Whenever we talk about well legally defined terms like assets, liabilities, and, you know, even property rights and ownership, our colleagues in the legal department and the lawyers who know this stuff well always kind of perk up, so we try to keep things conceptual in our thinking. Clearly data about individuals and data about companies is valuable. How valuable it is, is extremely difficult for some of the reasons that we’ve already discussed in the Q&A. The fact that if the data market is not complete, then the prices that you are currently observing for how much people are paying, how much companies are trading or paying to acquire another to obtain their data sets, these prices are not a reflection of how much it is worth because then the people who are involved who are affected by the transaction are not actually participant or are not fully participating. And so I think it’s quite misleading to equate the transaction prices that we’re seeing currently as being a true reflection of the full value of data. I think that’s that that’s one thing that needs to be kept in mind.

Vikram Haksar, Assistant Director, Macro-Financial Analysis – Financial Services, IMF

You know, Nasir I remember one of the events that we had invited you to, you stunned the audience by saying the value of your data? I think you said it was something like 100 bucks or something like that?

Nasir Zubairi, CEO of the LHoFT

130 bucks on average.

Vikram Haksar, Assistant Director, Macro-Financial Analysis – Financial Services, IMF

And so Yan I laid out the point that the incompleteness of the market makes it very hard to discern. Maybe what you Google pays for an ad every time you click or whatever. But I think for the public policy perspective, the other thing that we’ve grappled with in terms of asset and valuation, is the question about individual value, the intrinsic value of data versus the derived value. And I think that’s a big public issue that has to be tackled head-on, because there’s a lot of political momentum for arguing that data is an individual thing, that it is individually valuable and is being exploited. Right. And you got to move for example, in California with some of the new legislation there was discussion about having a data dividend that people should be required to be paid by the data from data processing companies.

And I think the other thing we’ve been to bear is, where do you draw the line? Let’s say you are buying a company which is incurring the costs of aggregating and accumulating all this information, and then processing it in house, with your knowledge about how to process it, to produce a product. How much is that the value of that product is the value of all the work that the company has done, as opposed to the value of the individual pieces of data that have been provided? Actually, we want to discuss with our lawyers some more. We wonder whether there are parallels from the jurisprudence of royalties, how you pay for royalties and use of intellectual property, for example, with some analog that could be brought over. But we think that this is a very difficult question, but one that is quite central. Maybe taking a little bit of the politics out of it. It can be a very emotive discussion.

Nasir Zubairi, CEO of the LHoFT

Thank you. Sorry for the difficult question. And while we’ve got one last question, I’m sorry, I know that there’s a number here, but I’m trying to do these in order. So we have a great question here. From Jose Bello.

Jose Bello, Co-Chair of IAPP KnowledgeNet Luxembourg

So my question would be regarding the situation that we’re all living right now here in Europe and across the world, of course. And I would like to put this question out: how do you see data and data-driven decisions making an impact towards the faster or slow recovery of Europe? Let’s not forget that we have the GDPR here. And I’m all for the GDPR as a privacy professional, but can data and not just personal data, also non-personal data, provide a boost to the economy with the current recession that we’re living on regarding with the COVID-19 and if you do have a specific example that you can think of, that be wonderful. Thank you so much.

Vikram Haksar, Assistant Director, Macro-Financial Analysis – Financial Services, IMF

“Advanced economies can learn from the implementation, and the leapfrogging that emerging and developing countries have done with the use of mobile payments and other types of digital and financial technologies.”

So my view on this, I think is that data and digitalization, I was saying Nasir before we started the call, that we’ve always been excited about digitalization and Fintech, we’re huge supporters of the work that LHoFT has been doing as well. And we are, you know, this is the future, this is where things are headed, and we should be ahead of it. And my joke was that, well, the future is now and frankly COVID in some ways brought a lot of these things forward. And one other point I would make is that I think that a lot of lessons that can be that advanced economies can learn from the implementation, and the leapfrogging that emerging and developing countries have done with the use of mobile payments and other types of digital and financial technologies, the network disaggregation, and the data to provide financial services and large populations very quickly. I think this is going to become quite critical for the recovery in Europe and other parts of the world.

Let me give you two examples. We just had a private discussion with some of the leading Chinese FinTech companies, that was an in house thing that the fund organized. So I speak under the rules, you know, we’re not allowed to talk about individuals and reveal too much detail. But the general sense was that, you know, in China, they’ve had the act of Fintech providing and leveraging big data from payment services and other products to provide credit analysis and very rapid financing. And the argument that the colleagues in the session were making was that they had found that while there had been some drop off during the lockdown that they have been able very quickly to resume credit and credit operations. And that not only credit and credit operations in general but credit especially targeted at small and medium business, which is a huge gap in most of the existing programs that are there, whether you’re talking about funding for lending or the other programs, the UK is advancing the problem, the Small Business Administration lending in the United States, the coordination and information problems with these programs is very large.

I think what you find is that in economies where they already have systems using technology to make the credit decision, and pipes to get the money out there, they are very effective. It’s gonna be a really interesting experiment to see whether recovery is fast. We know that small businesses actually, in most economies employ a very large share of the total population. That was one point. The other point is that data related to that is that this is the last mile problem. The piping of getting government aid out to individual households and businesses is very good at the top of the pyramid. So to get money out to financial intermediaries or financial institutions, central banks that know how to do that deployed very effectively, really fast this time around. But how do you get money out to individual households? How do you get money out to small businesses? I talked about small businesses already. But we think that to get money out to small households, for example, we’re going to see increased utilization of digitalization-based services, by ministries of finance, leveraging things like mobile, AP, P2P, that type of service to get money into the hands of individuals. The United States, one of the most sophisticated economies in the world, the fact that it takes four weeks for an IRS check, literally a physical check, to show up at somebody’s house with 500 bucks, I think is a real issue. So to answer your question, I think the bottom line is that this is a moment where we will see an acceleration of adoption of these technologies and great interest in the part of the official sector of actually seeing whether we can use more of these technologies to deliver public services and directed aid, faster, more effectively.

Yan Carrière-Swallow, Economist, Macro-Financial Analysis – Financial Services, IMF

“I think there’s probably less we can learn from pre-pandemic data than there would have been otherwise. So this is a moment of kind of structural break in a lot of relationships.”

I’d like to say something maybe that’ll sound a little bit conceptual and convoluted. I think it’s important at this point. So AI-ML is really about predictions, right? It’s about honing prediction models to try to infer what will happen in the future based on careful analysis of the past. And of course, we know that AI-ML has been very effective. A large number of applications have been scaled up across sectors. But I think one thing to keep in mind is that the basis of that technology is the continuity between the past and the future, if that link is broken, so if you live in a time where people start living differently, people start interacting differently. People go about their day differently. People make different decisions differently. Data you collected about the past, there’s going to be less informative about the future.

I agree with everything that Vikram said in the sense that data collection and data-driven decision making is going to be important in the recovery. But it’s important to keep in mind what data is going to be the key input to that, I think it’s gonna have to be the new data that we collect now, right, I think there’s probably less we can learn from pre-pandemic data than there would have been otherwise. So this is a moment of kind of structural break in a lot of relationships. And I think that needs to be kept in mind for all these data-driven decision-making processes.

Nasir Zubairi, CEO of the LHoFT

And we’ve gone over time, but it’s such a fascinating discussion, genuinely, very enjoyable. We have a host of other questions waiting, but we’ve just run out of time here. This is a bit awkward with web speakers. What I would normally ask people is can we have a round of applause for Yan and Vikram, but I can hear virtual applause all around me, gentlemen.

A real pleasure talking to you, it was fantastic to catch up with you both again. I hope we can do this again sometime soon. Now that the world is a smaller place with this technology, we’re all heading off in the next few minutes to FinTech Friday. You both are welcome to join us if you also free but I know it’s the middle of the day for you still. And I’m sure there’s plenty of important work to be done. But thank you all again for being there. Thank you all those that listened in. I enjoyed it a great deal. Thank you.